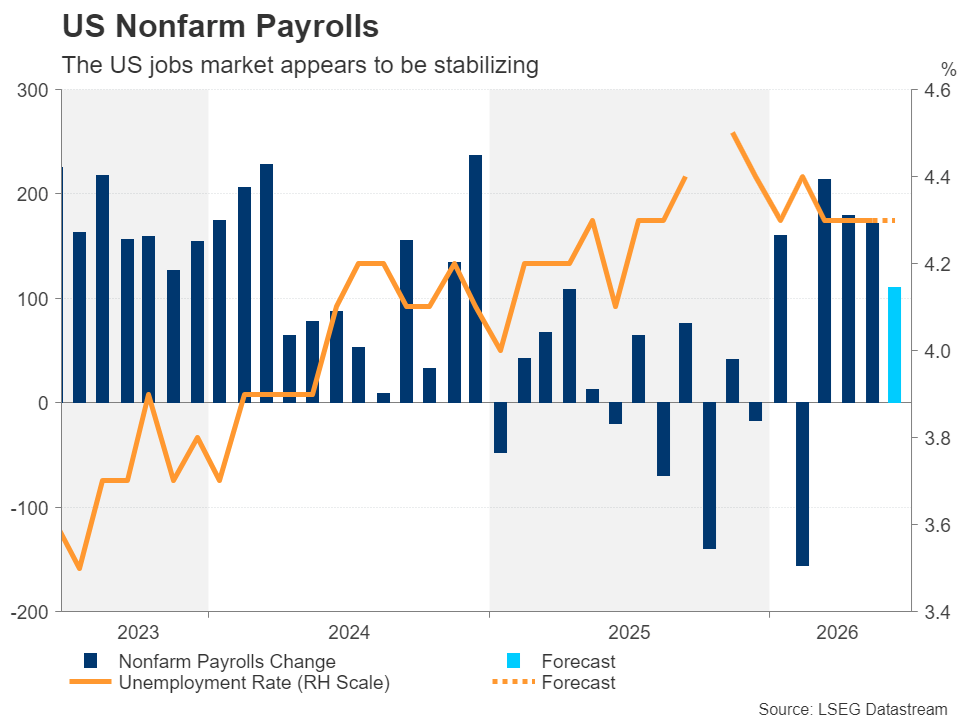

- The US labor market probably decelerated in June, although the World Cup could influence the figures.

- Warsh’s inaugural appearance at the Sintra forum is expected to be pivotal for the US dollar.

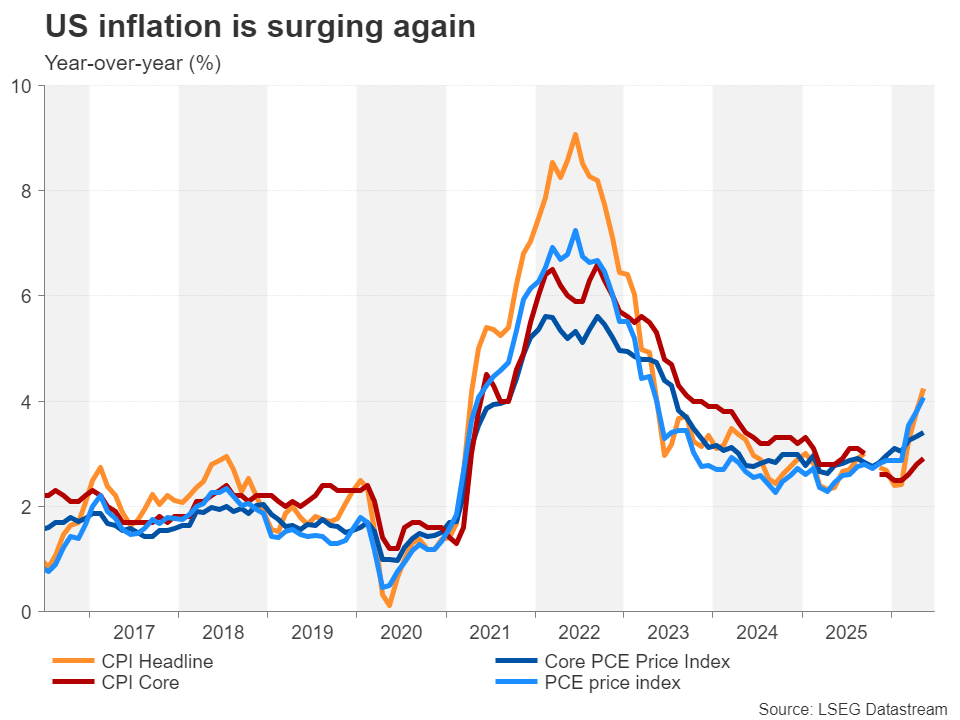

- Following the unexpected June FOMC outcome, the extent to which hawkish expectations will be met remains uncertain.

- Warsh is scheduled to speak on Wednesday at 13:00 GMT, while the non‑farm payrolls report will be released a day early on Thursday at 12:30 GMT.

A Barrage of Data and Central Bank Speak

Investors face a packed schedule this week, with the latest jobs report scheduled for release a day early because financial markets will be closed on Friday for Independence Day. Adding to the focus, Federal Reserve Chair Kevin Warsh will speak for the second time since assuming leadership, alongside a series of other US economic indicators that may influence expectations for future monetary policy.

Ahead of these risk events, market participants are moderately hawkish, assigning a probability of slightly more than two‑thirds to a 25‑basis‑point rate increase in September. This reflects a modest pullback from the near‑certainty of a hike that prevailed immediately after the June policy meeting. Nonetheless, markets have clearly understood Warsh’s emphasis on curbing inflation, indicating that any forward guidance will be limited.

Deciphering the New Fed Chair

The forthcoming data releases increase the likelihood of heightened market volatility, as investors examine every indicator while uncertainty persists regarding which metrics the Fed will prioritize under its new leadership. Wednesday’s panel discussion in Sintra, Portugal, organized by the European Central Bank, offers Warsh a platform to elaborate on the Fed’s strategy for returning inflation to its 2% target.

Given that other central bank officials—including Bank of England Governor Andrew Bailey, Bank of Canada Governor Tiff Macklem, and European Central Bank President Christine Lagarde—are also slated to participate, Warsh may be reluctant to disclose substantially new insights beyond what he conveyed at his post‑meeting press conference two weeks ago. Moreover, there is a risk that his tone may be less hawkish than during his debut at the FOMC, possibly mirroring the recent neutral stance adopted by New York Fed President William Dudley regarding future interest‑rate moves.

Is Another Hot NFP Report on the Cards?

If the earlier assessment proves accurate, any upside surprise in Thursday’s jobs report is likely to elicit a restrained market response. After May’s stronger‑than‑expected reading of 172,000 jobs, economists now project a more modest increase of 110,000 for June. The unemployment rate is expected to remain unchanged at 4.3% for a fourth consecutive month, while average hourly earnings are forecast to rise marginally to 3.5% year‑over‑year.

A headline figure that exceeds expectations could further intensify speculation about a September (or even July) rate hike. Such an outcome appears plausible given the decline in energy prices following de‑escalation in the Middle East and the economic boost from hosting the FIFA World Cup, which together may have spurred additional hiring in June.

Choppy Times Ahead for the Dollar

For the US dollar, the period leading up to Thursday’s jobs release will be fraught with complexity. In addition to the ECB forum and the NFP data, market participants will need to monitor the June consumer sentiment index, the May JOLTS job‑openings report on Tuesday, as well as the June ISM manufacturing PMI, ADP employment figures, and Challenger job‑cut statistics—all scheduled for release on Wednesday.

Simultaneously, any developments in US‑Iran negotiations could provide additional tests for dollar bulls, alongside further commentary from other central bankers at Sintra. Notably, the euro will remain in sharp focus, especially if Lagarde signals a more optimistic outlook for Eurozone inflation, buoyed by oil prices that have largely returned to pre‑war levels.

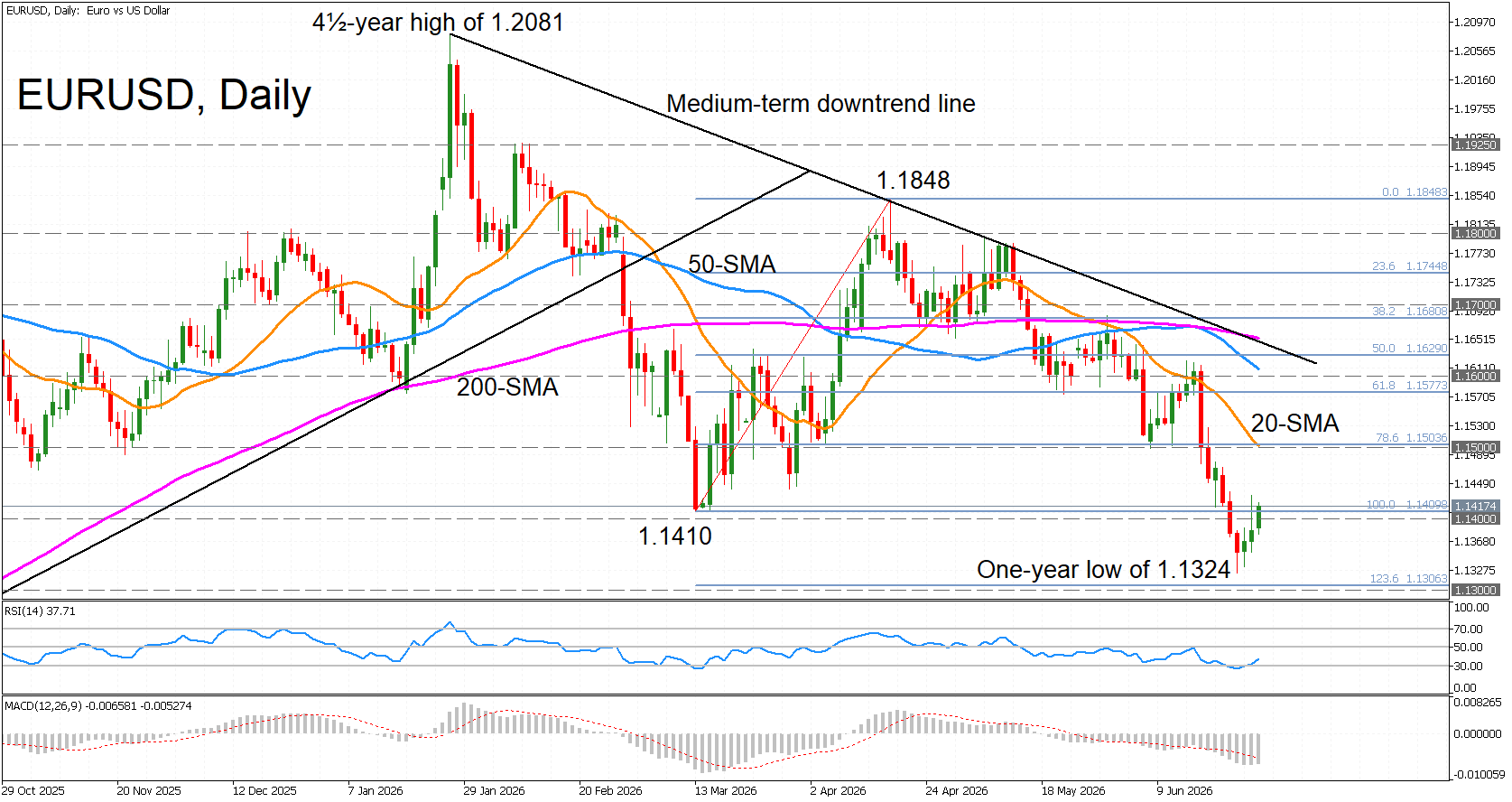

Is the Euro in Danger of Breaching $1.13?

Despite the easing of geopolitical tensions, these factors have not been sufficient to counterbalance the dollar’s strength stemming from the Fed’s hawkish stance. The euro previously hit a one‑year low, briefly dipping below $1.1400. A favorable set of US labor‑market data would further reinforce expectations of a hawkish policy, potentially prompting renewed selling pressure toward $1.1300, a level that aligns closely with the 123.6% Fibonacci extension of the March‑April price rebound.

Conversely, weaker-than‑expected NFP figures together with a more subdued tone from Warsh could support the euro, lifting it toward its 20‑day moving average, which sits just above $1.1500.

Wall Street will continue to scrutinize both Warsh’s commentary and the upcoming payroll data. The recent formation of a lower high in the S&P 500 indicates that the recent AI‑driven rally may be losing momentum. A hot jobs report would therefore pose a significant obstacle to achieving a new all‑time market high, as it would likely solidify expectations for a September rate hike.

Also Read

- XRP Exodus from Binance Signals Market Bottom as Ripple’s Stablecoin Expands in Indonesia

- QuantRate Democratizes Automated Investing with New Free AI-Powered Multi-Asset Trading Platform

- Crude Prices Rebound to Pre‑Conflict Levels Amid Market Adjustment

- USD/CAD Market Outlook: Consolidation and Potential Upside in Sight