USD/JPY has resumed its upward trajectory as the most likely window for Japanese foreign‑exchange intervention passed without any official action. The pair rose after a brief dip caused by last week’s intervention speculation, supported by a dollar rebound and the market’s absorption of the June non‑farm payrolls’ dovish surprise. Meanwhile, the yen’s temporary premium tied to intervention fears has now faded.

Last week’s yen strength was rooted in a rapid shift in market psychology. Reports that Japan might skip its customary warning cycle and intervene without notice created a sudden‑strike risk, amplified by thin liquidity over the US holiday week and the quiet Asian session that followed. In those conditions, any direct yen buying could have produced an outsized market impact.

The surge proved short‑lived because it was driven not by fundamentals but by a positioning squeeze. Traders had built up short‑yen bets fearing that Tokyo would exploit the holiday‑period liquidity to force a sharp reversal. With the window passing without intervention, the associated risk premium vanished, letting the dollar‑yen pair recover above 162.

The episode mirrors earlier Japanese interventions, which typically occurred during holiday or low‑liquidity periods when official buying could have a magnified effect. The April‑May precedents underscored the importance of the recent Friday‑to‑Monday window. Its uneventful outcome was interpreted by markets as a cancellation of the near‑term intervention risk, not just a delay.

As a result, the underlying trend resumed. While June’s payrolls softened enough to temper expectations for aggressive Fed tightening, they did not spark a shift toward rate cuts. The market still prices one Fed hike in 2024, and the BOJ’s policy remains far below US rates, keeping carry trades active and providing upward pressure on the yen whenever intervention concerns ease.

However, Tokyo’s threat retains some credibility. A move toward 162‑165 could still trigger intervention, particularly if the advance becomes disorderly. Nonetheless, intervention is now best seen as sporadic and event‑driven, capable of temporarily stalling the trend around holidays, low‑liquidity periods, or key psychological levels, but it has not altered the broader structural outlook.

In the broader currency arena, the dollar leads the session, followed by sterling and the Australian dollar. The yen lags, trailed by the kiwi and the Swiss franc, while the euro and loonie sit in the middle. Market participants are now pricing out the recent intervention speculation and refocusing on the wide policy differential between the Fed and the BOJ, keeping USD/JPY’s larger uptrend intact.

Gold Finds Support at $4,000, but Only Softer Inflation Can Fuel the Next Rally

Gold’s recovery from the $4,000 level is stalling as traders shift focus from softer payroll figures to upcoming inflation metrics. With market participants still pricing the possibility of another Fed rate increase this year, the July CPI report will likely dictate whether the metal can break higher or revert to its broader downtrend. The analysis covers the macro environment, Fed outlook, and key technical thresholds.

NZD/USD Bears Await RBNZ Verdict After Relief Rally

NZD/USD is entering a pivotal week as the Reserve Bank of New Zealand weighs its dual mandate of curbing inflation and supporting economic growth. Market participants are split on whether the Official Cash Rate will be increased, with many believing the policy statement could carry more weight than the rate decision itself. This coverage analyzes the divergent views, their implications for the kiwi, and the technical levels that hint the recent bounce may prove short‑lived.

Eurozone Sentix Investor Confidence Surges to -3.1 as Germany’s Recovery Gains Traction

Eurozone investor confidence rose for the third straight month in July, supported by an improved German outlook and diminishing inflation concerns. The Sentix survey points to a more broad‑based recovery across the bloc, which lessens the urgency for additional ECB tightening.

Eurozone Producer Inflation Holds Firm as Core Factory Prices Continue to Rise

Eurozone producer price inflation accelerated faster than anticipated in May, driven by robust gains in intermediate goods and a steady rise in core factory prices, which compensated for lower energy costs. The most recent PPI data shows that underlying pipeline inflation remains firm despite a moderation in headline monthly growth.

Eurozone Retail Sales Rise 0.2% mom in May as Food Spending Leads Growth

Eurozone retail sales matched expectations in May, with growth driven primarily by increased spending on food and non‑food items, while fuel sales weakened. Overall consumer demand stayed resilient, though the performance was uneven among member states, underscoring the divergent nature of the regional recovery.

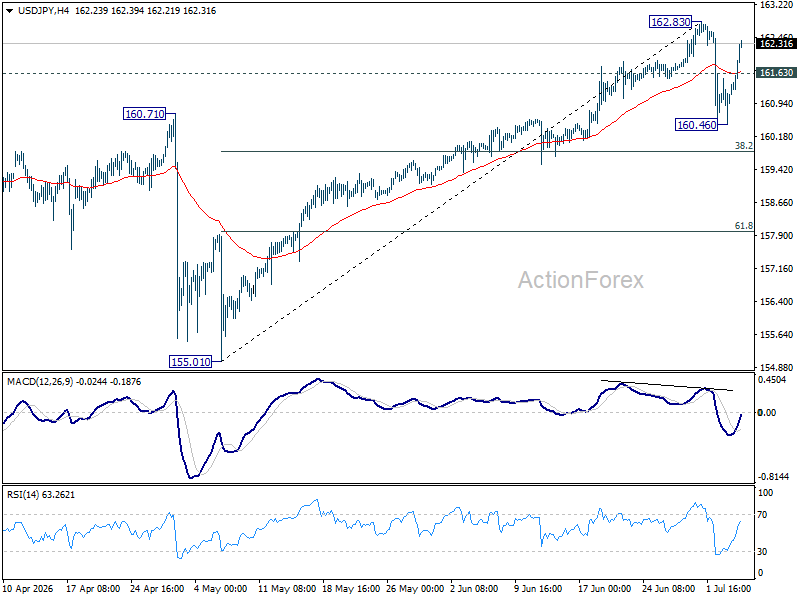

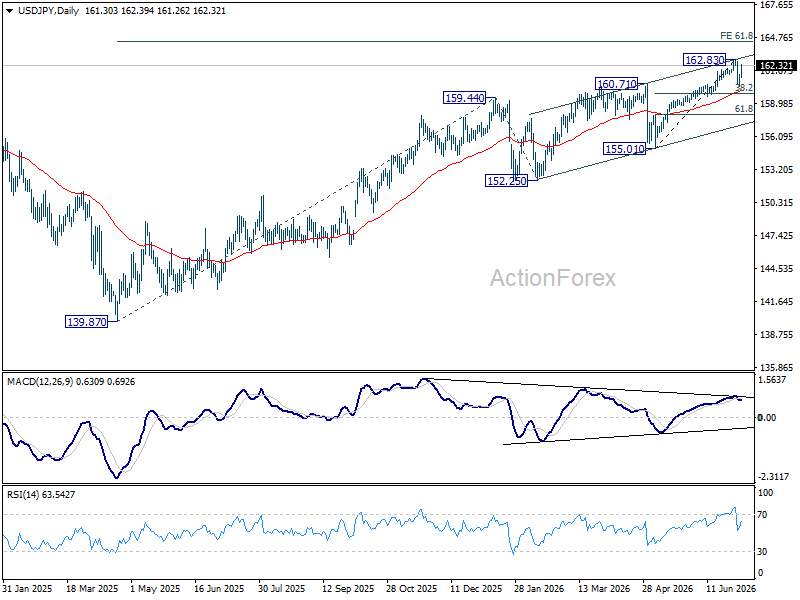

USD/JPY Daily Outlook

The immediate bias for USD/JPY is neutral following the recent strong rebound. While consolidation below the 162.83 level is possible, any further decline is expected to find support near the 38.2% Fibonacci retracement of the 155.01–162.83 move, around 159.84. A confirmed break above 162.83 would re‑ignite the broader upward momentum.

Looking at the longer term, the rise from the 139.87 low (2025) appears to be a continuation of the established uptrend. The next projected target is the 61.8% extension of the 139.87–159.44 move from the 152.25 swing, set at roughly 164.34. As long as the 155.01 support holds, the overall outlook remains bullish, even if a deeper correction occurs.

Economic Indicators Update

GMT CCY EVENTS Act Cons Prev Rev

01:00 AUD TD-MI Inflation Gauge M/M Jun -0.40% -0.30%

06:00 EUR Germany Factory Orders M/M May 1.90% 1.10% -3.80%

08:00 CHF Unemployment Rate Jun 3.10% 3.10% 3.10%

08:30 EUR Eurozone Sentix Investor Confidence Jul -3.1 -8.9 -13.4

08:30 GBP Construction PMI Jun 38.4 40.1 38.2

09:00 EUR Eurozone Retail Sales M/M May 0.20% 0.20% -0.40%

09:00 EUR Eurozone PPI M/M May 0.20% 0.20% 0.60% 0.70%

09:00 EUR Eurozone PPI Y/Y May 5.90% 5.70% 4.90% 5.00%

13:45 USD Services PMI Jun F 51.4 51.3

14:00 USD ISM Services PMI Jun 54.2 54.5

14:00 USD ISM Services Prices Paid Jun 71.3

14:00 USD ISM Services Employment Index Jun 47.9