Canadian Highlights

- Markets reacted to hopes of a Middle East cease‑fire, yet the outlook stays uncertain.

- Canada’s economy has stalled for two consecutive quarters, driven by weak domestic demand and uneven investment, resulting in muted growth momentum.

- The forthcoming CUSMA review is now a focal point as Canada seeks clearer trade terms alongside an energy‑focused investment strategy.

U.S. Highlights

- Optimism over a potential U.S.–Iran cease‑fire extension pulled WTI crude down 9% this week, to $88 per barrel.

- Consumer spending held steady in April despite rising inflation and shrinking household savings.

- A growing number of Fed officials are signaling a more hawkish stance, with futures pricing a roughly 60% probability of a rate hike by year‑end.

Canada – Canada’s Economy Stalls Ahead of Trade Negotiations

Hope for a peace agreement between Iran and the United States, aimed at reopening the Strait of Hormuz, dominated market sentiment this week. Although optimism about a potential 60‑day truce drove oil prices lower by about nine percent, volatility remains high. Rapid market reactions to evolving headlines highlight the fragile outlook. For Canada, this volatility coincides with lingering uncertainty over U.S. market access, exerting pressure on domestic activity.

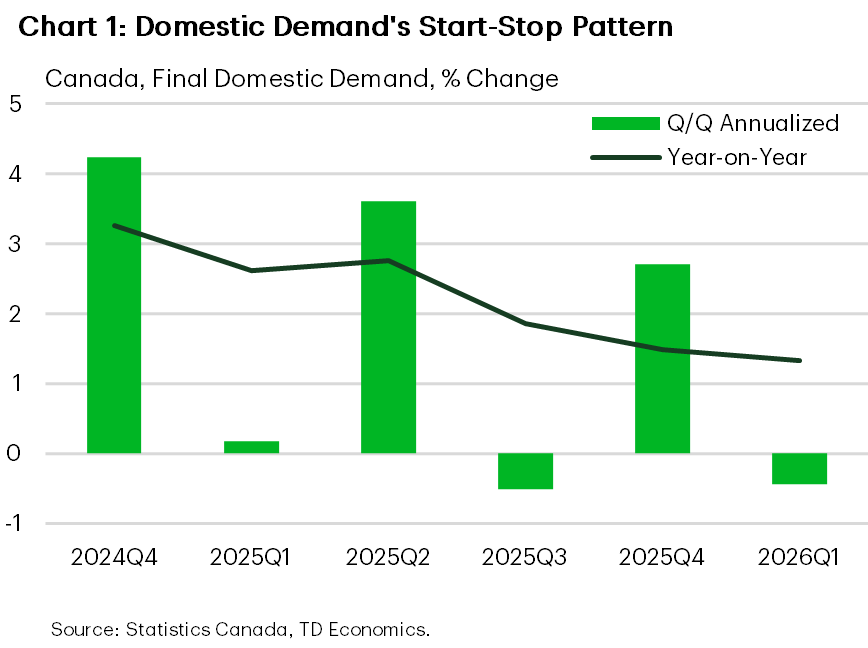

The first‑quarter GDP report indicated a modest contraction of 0.1% quarter‑on‑quarter, annualized, marking a stall that fell short of expectations. Weakness was widespread. While strong import growth depressed the headline figure, final domestic demand fell 0.4% quarter‑on‑quarter, remaining uneven and inconsistent. Despite volatility, domestic demand is up 1.3% year‑on‑year, though still below trend and indicative of an economy operating below capacity.

Household spending rose 1.5% quarter‑on‑quarter, propelled by services, though the pace slowed relative to Q4. Investment growth in machinery, equipment, and intellectual property was offset by a sharp decline of 7.9% quarter‑on‑quarter in residential investment and weaker spending on engineering structures. Government investment, which had risen in late 2025, receded in the quarter.

Overall, the economy is progressing with limited forward momentum. Early Q2 signals hint at a modest rebound, as April GDP appears to be trending higher, yet the broader trend still reflects slack and subdued growth.

Canada’s sluggish growth has shifted attention to the upcoming CUSMA review. Uncertainty over U.S. market access, dating back to the initial tariff tranche announced last year, continues to weigh on the economy. On Monday, the three nations are expected to exchange their proposed amendments to the agreement, followed by formal negotiations. The United States and Mexico have already set up negotiating rounds. Trade Minister Dominic Leblanc is slated to travel to Washington next week, though the negotiation timeline remains uncertain.

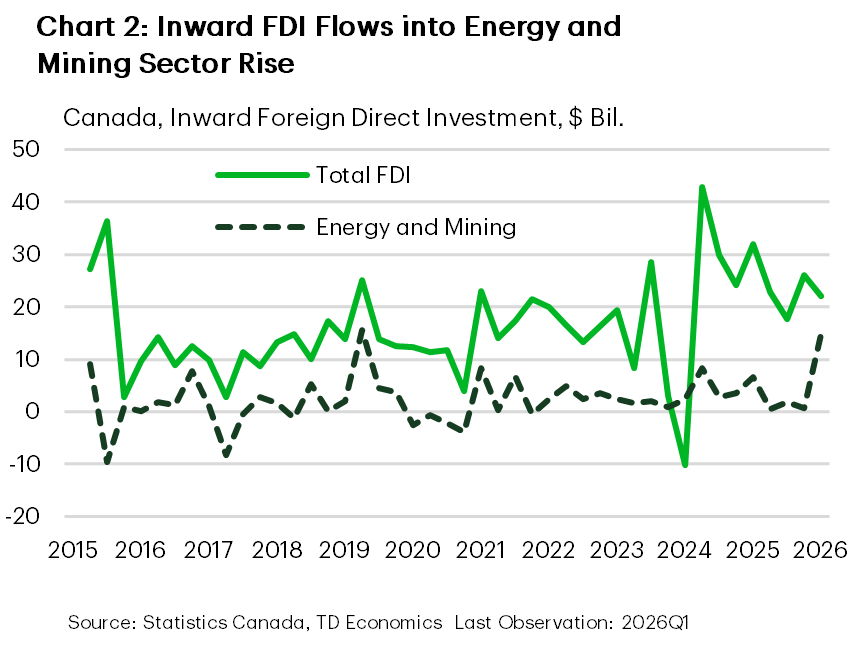

To gain insight into the negotiations, Prime Minister Mark Carney’s speech in New York this week outlined Canada’s strategy. He advocated for a “new partnership” with the United States and emphasized the nation’s ambition to become an “energy superpower.”

Recent foreign‑direct investment figures lend some support to the strategy. Q1 inflows totaled $22 billion, about $4 billion lower than the previous quarter, with $14.7 billion allocated to energy and mining sectors. Although the data are volatile, they align with Canada’s plan to capitalize on its resource base and attract long‑term capital.

The Canadian economy remains constrained by trade uncertainty. Prospects for clearer and more stable relations with the United States in the coming months could boost confidence. Greater certainty, together with efforts to attract global capital into Canada, may provide a base for productivity‑driven growth.

Canada – Canada’s Economy Stalls Ahead of Trade Negotiations

Three months after the United States began its initial operations against Iran, hopes for a durable peace agreement have risen this week following President Trump’s remarks that a deal was “largely negotiated.” Oil prices dropped sharply in response, although brief renewed attacks mid‑week momentarily dampened optimism. By Thursday evening, reports indicated that the parties had reached a 60‑day memorandum of understanding to extend the ceasefire, pending the president’s approval. Oil prices fell 9% over the week, with WTI trading around $88 per barrel. Economic data released this week showed a cautious yet resilient consumer sector amid renewed inflationary pressures. The S&P 500 rose 1.3% for the week, while the 10‑year Treasury yield slipped 12 basis points to 4.44%.

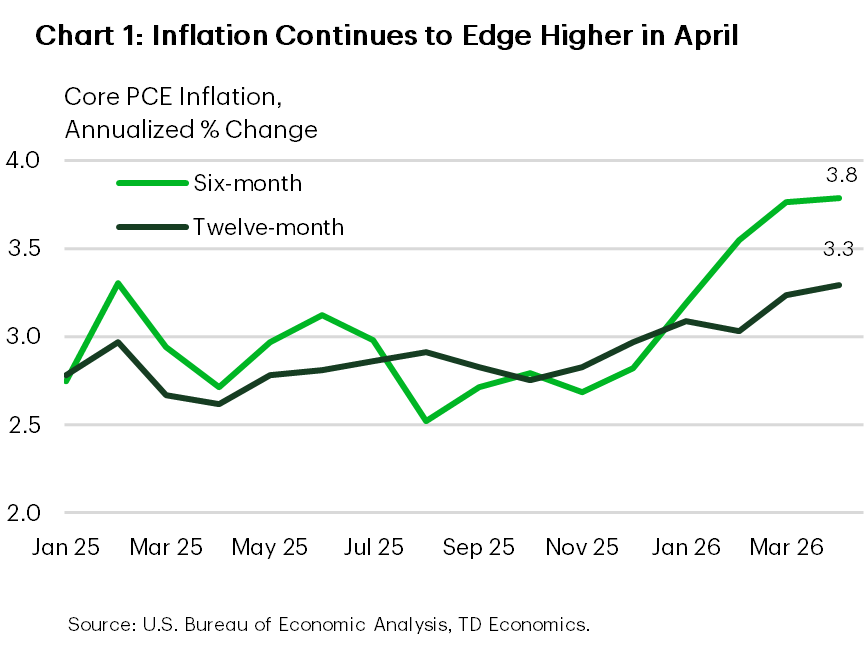

This week’s release of the April personal income and spending report highlighted the strain on American households from the recent energy shock. Core personal consumption expenditures (PCE) inflation climbed to a three‑year high of 3.8% year‑on‑year, and is expected to exceed 4% in May as gasoline prices rise. Excluding food and energy, core PCE inflation edged up to 3.3%. Both three‑month and six‑month measures have risen to 3.8% (see Chart 1).

Despite higher inflation, consumer resilience has held. Nominal spending increased 0.5% month‑over‑month in April, after a 1% rise in March. Adjusted for inflation, the April gain was modest—about 0.1% month‑over‑month—but still positive. Persistent inflation is eroding purchasing power, causing real disposable income to fall for a third straight month. With the savings rate at a four‑year low, households have limited cushion for spending.

A recent Conference Board survey indicates softer spending intentions ahead. Fewer households intend to buy big‑ticket items, and two‑thirds of consumers plan to cut overall spending because of rising prices. Although post‑pandemic survey metrics have been less reliable, the signal cannot be dismissed. The energy shock has further pressured affordability for lower‑ and middle‑income households, who have not enjoyed the same home‑price and equity gains seen in previous years.

Affordability pressures are likely to intensify if the energy shock persists. A growing chorus of Fed officials is becoming more hawkish as inflation remains elevated. Board member Lisa Cook warned that if disinflation does not resume soon, she is “prepared to raise rates.” Fed President Kashkari reiterated that combating inflation remains the priority, given the labor market’s improving shape. Consequently, next week’s employment data may take a backseat to the May CPI release scheduled for June 10. Fed futures now price a 60% probability of a rate hike by year‑end, though a hotter inflation reading could shift expectations forward.

Also Read

- Franklin Templeton Files for ETFs That Convert Corporate Dividends into Bitcoin Exposure

- Japanese Yen Nears 40-Year Lows as Intervention Speculation Rises

- Europe’s MiCA July deadline puts Binance access and USDT liquidity on the line

- USD/CHF Price Forecast: Fails ahead of 0.8100/YTD peak; bullish potential intact