The dollar concluded the week without a clear trajectory, even as U.S. inflation data revealed a more pronounced easing trend. June’s Consumer Price Index (CPI) and Producer Price Index (PPI) both registered significant month‑over‑month declines, underscoring the view that broader price pressures are loosening. Rather than continuing to weaken, the greenback steadied as investors weighed whether this disinflationary momentum will hold beyond a single month.

This caution stemmed from a second, forward‑looking event: a sharp uptick in the U.S.–Iran conflict that pushed crude prices higher. Brent closed above $88 and West Texas Intermediate (WTI) recovered the $80 mark. With June’s soft figures largely driven by lower energy costs, the sudden rebound in oil lifted concerns that inflation could reaccelerate in the near term. Markets shifted focus from past easing to potential future tightening.

The outcome was a currency market caught between contradictory forces. Soft inflation reduced pressure for further Fed tightening, but higher oil prices revived the risk of a new inflation surge, keeping rate‑hike expectations afloat. This duality appeared in currency movements: the New Zealand dollar led gains, followed by the Canadian dollar and sterling, while the yen weakened most. The dollar hovered nearPutting myself actually? Actually / sits near the mid‑range, reflecting the market’s continued assessment of yesterday’s disinflation against tomorrow’s risk.

Soft CPI and PPI Shifted the Fed Outlook—Temporarily

June’s inflation releases added to a growing consensus that U.S. price pressure is easing. CPI fell 0.4% from the 0.5% rise in May, lowering the year‑over‑year rate from 4.2% to 3.5%, well below expectations. Core CPI remained flat, with the annual rate slipping from 2.9% to 2.6%. At the producer level, PPI slipped 0.3% month‑over‑month—its steepest decline in over six years—further confirming a slowdown in upstream inflation transmission.

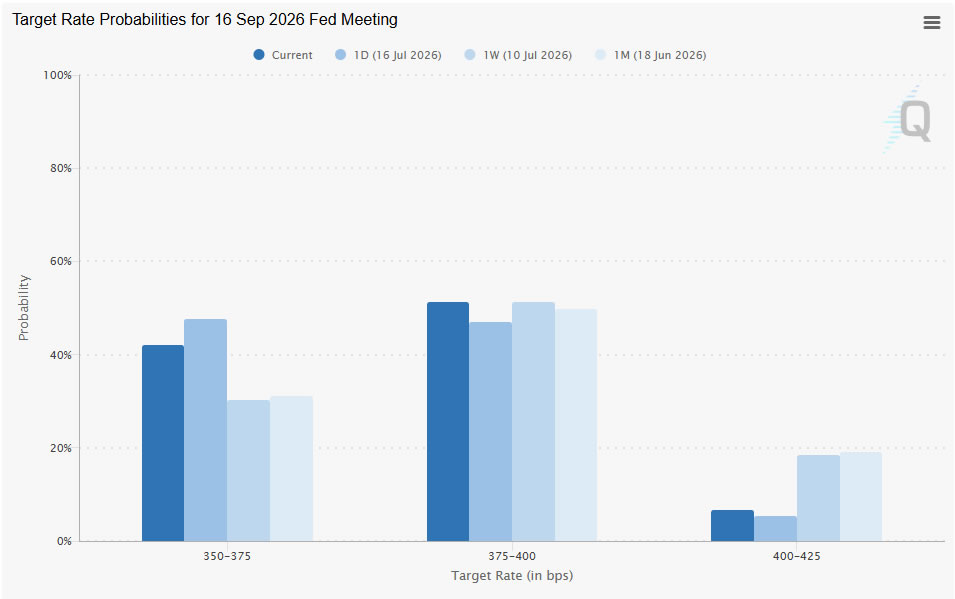

The breadth of this contraction suggested it was not a statistical blip. A back‑to‑back fall in both consumer and producer prices prompted investors to reassess the urgency of additional Fed tightening. Favored futures adjusted quickly, with the probability of a September rate increase dropping from roughly 70% to about 58% in the days following the data.

Nonetheless, the data’s composition raised caution. Lower gasoline prices, which significantly underpinned the CPI and PPI decline, mirrored a brief lull in Middle‑East tensions that lifted markets and reduced energy costs. As prices later climbed, the June relief appeared precarious, reinforcing the narrative that the disinflation story, while credible, was fragile hinging on volatile energy dynamics.

WTI Above $80 Changes the Inflation Narrative

The week’s pivotal development may ultimately be the sharp rebound in oil rather than the softer inflation figures. The escalation between the U.S. and Iran escalated concerns about energy supply, with strikes targeting critical infrastructure across the region and Iranian retaliation expanding to Gulf partners and a U.S. base in Syria. Consequently, WTI surged above $80 and Brent crossed $88, recording the largest weekly gains since April.

WTI’s recovery above the $80 threshold is significant because June’s disinflation was largely driven by a temporary dip in energy costs amid a brief respite in Middle‑East tensions. With crude now back at the highest levels in months, the energy component of inflation isיינים poised to rise, undermining the durability of June’s gains.

This shift explains why expectations for another rate hike did not dissolve, despite the soft data. Investors are moving from a focus on June’s numbers to assessing July and August inflation risk if oil prices remain elevated. Energy markets, therefore, now dominate Fed setback and, by extension, the dollar’s direction.

Fed Keeps the Door Open to Further Tightening

Federal Reserve officials continued to adopt a cautious, hawkish tone throughout the-authoritative week, even as June’s inflation figures came in softer than expected. In a Congressional hearing, Chair Kevin Warshasjon rejected the notion that the Fed’s work was finished, emphasizing that inflation was still too high. He also noted that monetary policy was “not particularly restrictive,” indicating 관한 the committee still possesses room toijet tightening if inflation risks rise again.

Governor Christopher Waller echoed this stance. Prior to inflation releases, he suggested that a new hike might be warranted in the near future somente CPI and PPI rose. Although the data lessened the immediτο case for further tightening, his remarks highlighted the Fed’s continued sensitivity to fragile inflation dynamics. Dallas Fed President Lorie Logan emerged as the most hawkish voice of the week, becoming the first official since Chair Warsh to publicly endorse another rate increase.

Overall, the Fed’s messaging did not shift markedly despite encouraging inflation reports. The committee acknowledged progress but remained hesitant to pre‑emptive disconnectrate hikes. Accordingly, policy decisions will likely be guided by incoming data—and, increasingly, by energy developments—rather than political rhetoric. Markets, therefore, are focused on whether rising oil prices may compel the Fed to adopt a more aggressive stance.

Technical Outlook: Dollar Awaits Confirmation from Oil করবে? and Yields

Brent crude

A decisive break above the 89/90 area would signal that Brent is already reversing its extended decline from 119.50. This would pave the way to a 61.8% retracement at 100.64, close to the 100 psychological level. If the speculator fails to clear 89–90 and breaks below 83.71, the rally may have been merely a corrective bounce, suggesting the recent uptrend has ended.

US 10‑year yield dipped to 4.51 but swiftly recovered after touching the 55‑day EMA (now 4.51). The prior correction from 4.69 to 4.36 has likely concluded, and the move upward from 3.96 appears to be resuming. A break above the 4.62 resistance would confirm the bullish stance, targeting a retest around the 4.62 high.

NASDAQ’s selloff on Friday and break of the 55‑day EMA (now at 25,634.10) signals that the consolidation pattern that began at 27,190.21 is extending with a new downward leg. Key support lies near the 38.2% retracement of the 20,690.25‑27,190.23 move, at about 24,707.22, which should contain downside and spur a rebound. A decisive break below this Fibonacci level would suggest a larger‑scale selloff, potentially pulling back to the 61.8% retracement at 23,173.23.

Dollar Index’s recent correction from 101.80 downwards has held above 38.2% retracement of 97.62‑101.80 at 100.20, as well as the 55‑day EMA (now 100.17). A further rally remains likely. A move above the 101.32 minor resistance would confirm the upward bias, prompting a retest of the upper 101.80 high. A firm break there could extend the full rise from 95.55 to the 110.17 high, while a sustained drop below the 55‑day EMA could signal a bearish reversal.

The dollar enters the new week still seeking a decisive catalyst. If the U.S.–Iran conflict continues to deepen, Brent is likely to breach the $90 barrier, reinforcing expectations that the recent disinflation trend could be short‑lived. Such a scenario would lift Treasury yields, strengthen pricing for a potential Fed rate hike later this year, and provide fresh support for the dollar.

Conversely, any meaningful de‑escalation that pulls oil prices back down would revive confidence that inflation is moving back on a downward trajectory, prompting markets to trim tightening expectations and create a broader case for dollar weakness.

At present, the escalation scenario appears slightly more probable. The increasing coordination of recent military operations and Iran’s widening retaliation indicate that the conflict is entering a more dangerous phase than earlier exchanges. Yet investors have learned that geopolitical developments can shift abruptly. Thus, the dollar sits at a crossroads, with its next major move likely determined less by Fed rhetoric or scheduled releases than by whether oil continues to rewrite the inflation outlook.

EUR/USD Weekly Outlook

EUR/USD continued its consolidation above 1.1323 last week, and the outlook remains unchanged. The initial bias for the week is neutral, and with the 1.1499 support now acting as resistance, further downward movement is anticipated. A break below 1.1323 would resume the previous decline from 1.2081. However, a decisive break above 1.1499 would re‑establish an upside bias toward the 1.1621 resistance.

In broader terms, focus shifts to the 38.2% retracement of 1.0176–1.2081 at 1.1353. A decisive break there would signal a medium‑term bearish reversal after rejection at the 1.2 cluster resistance. A further decline to the 61.8% retracement at 1.0904 could follow. A strong rebound from 1.1353 and a subsequent break of 1.1621 would maintain medium‑term bullishness.

In the long‑term view, the 38.2% retracement of 1.6039–0.9534 at 1.2019, close to the 1.2000 psychological level, is key. Rejection at this level would preserve the long‑term downtrend from 1.6039 (2008 high) and keep the outlook neutral. A decisive break of 1.2000/19 would suggest a long‑term bullish reversal, targeting the 61.8% retracement at 1.3554.

hundreds of images follow…

Also Read

- Quantum-Resistant Bitcoin Wallet Proof Offers New Recovery Path, Excludes Satoshi’s Holdings

- Wall Street’s Private Credit Crisis Brews Beneath the Surface

- Dutch Court Declares Bankruptcy for Crypto Exchange Knaken Amid MiCA Compliance Issues

- South Korea Launches Won Internationalization Initiative for Global Investors