- The Federal Reserve left policy unchanged at Kevin Warsh’s first meeting as Chair. While Warsh did not release personal projections, the overall committee outlook now leans more toward future rate hikes.

- The meeting marked a shift away from traditional forward guidance. Warsh stressed the Fed’s commitment to returning inflation to target and announced that communications and balance‑sheet policy will be reviewed by dedicated task forces by year‑end.

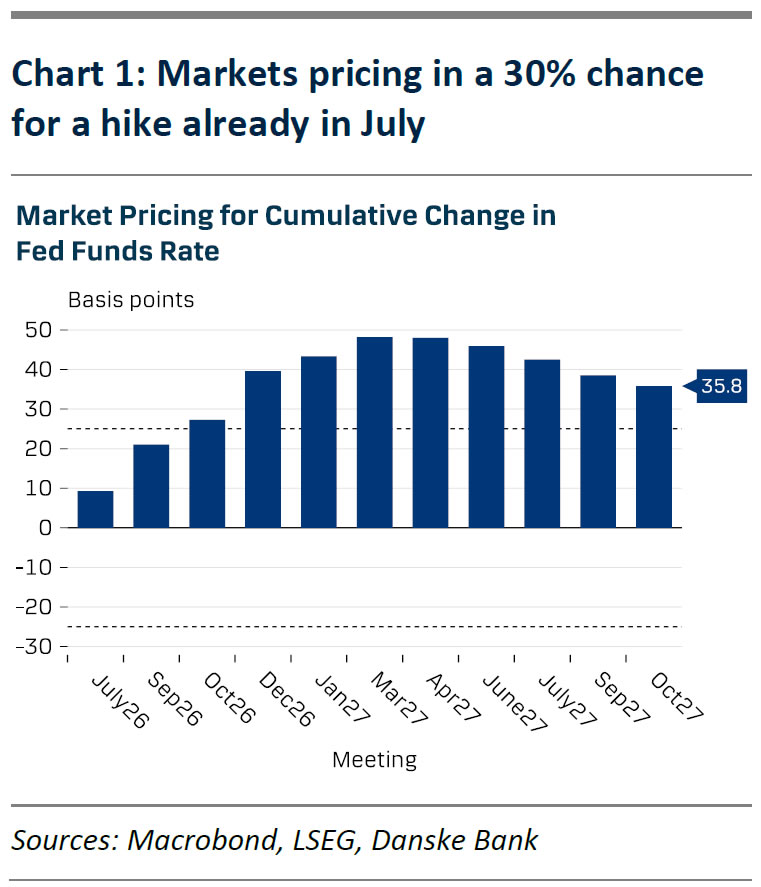

- EUR/USD slipped below 1.15, U.S. Treasury yields rose and the yield curve flattened as market pricing for the terminal rate moved up 17 bp. The market now prices a front‑loaded risk of hikes—8 bp by July and 20 bp by September. We continue to expect hikes in December and March, but acknowledge the possibility of an earlier start.

- Our recommendations to go long USD versus SEK and NOK, and to trade the 2‑year SOFR‑ESTR spread have performed well, and we remain supportive of all three strategies.

Kevin Warsh set a new tone for forward guidance—or its absence—by issuing a concise statement focused on three points: policy unchanged, ample reserves maintained, and a commitment to price stability.

During the press conference, Warsh avoided speculation about future moves and emphasized the Fed’s resolve to bring inflation down to 2%.

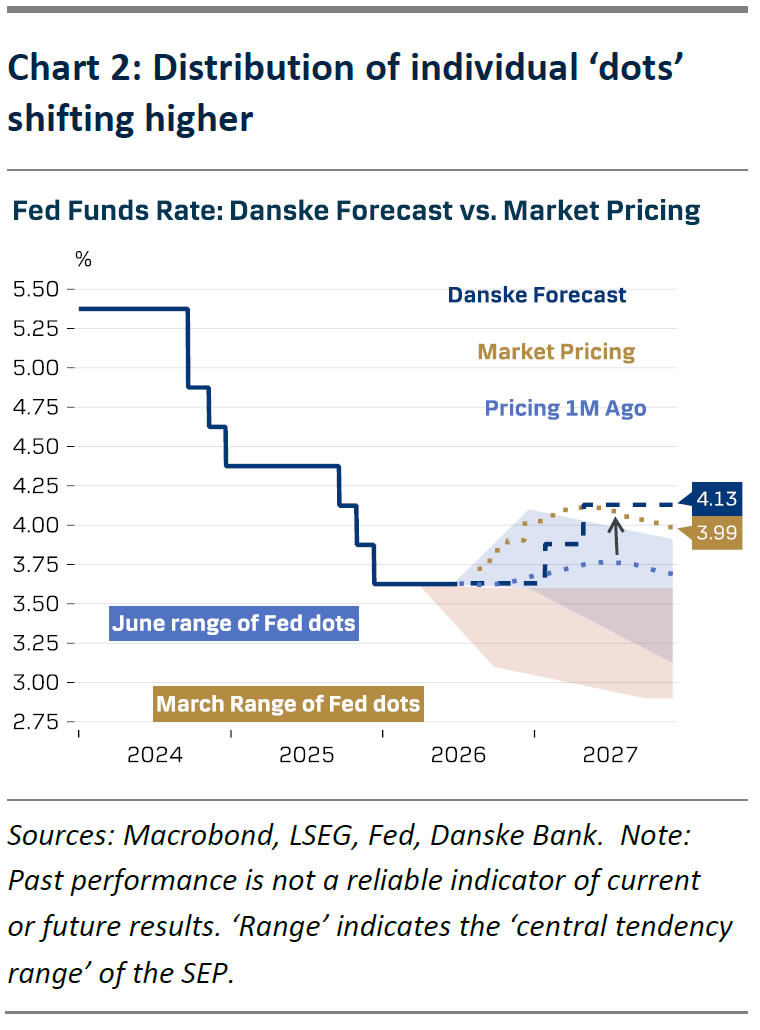

Although Warsh did not submit his own “dot plot,” he encouraged other members to continue doing so. Updated projections show a clearer hiking bias than our June 16 preview: only one participant favored a rate cut this year, eight saw rates unchanged, and nine projected one to three hikes. Median forecasts for 2027 and 2028 were lifted by 50 bp and 25 bp respectively. GDP and unemployment forecasts were largely unchanged, while core PCE inflation expectations rose to 3.3% in 2026 (up from 2.7%). The committee viewed risks to GDP and labor markets as balanced, while 17 of 18 members saw upside risks to core inflation, matching our expectations.

Warsh did not clarify whether the FOMC will continue publishing dot plots. He did announce five task forces to examine communications, balance‑sheet policy, data sources, productivity, and the inflation framework, with recommendations due by year‑end.

We maintain our outlook for two Fed hikes in the next year—December and March. However, stronger‑than‑expected macro data could push the first hike forward to September. We also expect the Fed to keep expanding its balance sheet through monthly Treasury‑bill purchases of roughly $10 bn.

Market Reaction

U.S. Treasury yields rose and the curve flattened as market pricing for the terminal rate increased by 17 bp. The market now anticipates nearly two full hikes over the coming year, with expectations front‑loaded—8 bp priced in for July and a cumulative 20 bp by September. Our 2‑year SOFR‑ESTR spread trade is currently 18 bp in the money. While we still favor the structural case, the tactical upside appears to be waning.

On the long end of the curve, expectations of tighter policy pushed breakeven inflation lower. Tighter financial conditions are likely to dampen growth, contributing to recent equity declines and weaker cyclical currencies. EUR/USD fell below 1.15, and we maintain our below‑consensus 12‑month forecast of 1.12. Our long‑USD positions versus SEK and NOK have performed well; we have added a trailing stop‑profit to the USD/NOK trade to lock in gains.

Also Read

- Upcoming Crypto Bull Market Expected to Be Gradual and More Stable, Says Bitwise CIO

- USD/JPY Surges to Two‑Year Peak on Hawkish Fed Outlook Renewing Rate‑Hike Speculation

- CME CEO Announces Intent to Sue CFTC Over Perpetual Futures Approval

- Japan’s Top Government Spokesperson Signals Readiness to Act on Yen Volatility