![Phillies Release Rene Pinto After Signing Payton Henry to Replace Him Behind Plate]](https://i0.wp.com/imageio.forbes.com/specials-images/imageserve/6a4e7b3c97716afa808c1d9f/0x0.jpg?format=jpg&crop=1469,826,x1297,y96,safe&height=900&width=1600&fit=bounds&w=1024&resize=1024,1024&ssl=1 "Phillies Release Rene Pinto After Signing Payton Henry to Replace Him Behind Plate]")

This week GBP/CAD surged to a decade‑high level, highlighting a growing gap between a pound that is gaining strength as domestic political risks subside and a Canadian dollar that is under pressure from structural factors. The pound’s rise follows the unwind of large speculative short positions that were established before Prime Minister Keir Starmer’s resignation, and Bank of England Governor Andrew Bailey has indicated that no rate cuts are expected in the near term. With the Bank of England’s rate at 3.75% compared with the Bank of Canada’s 2.25%, the yield differential remains substantial. Recently, the rally has been bolstered by heightened uncertainty regarding Canada’s trade prospects.

July 1 marked a pivotal moment when the Trump administration chose not to grant another 16‑year extension to the USMCA, even though the pact remains in effect through its annual review process. While the agreement continues for potentially another ten years, the decision introduces greater long‑term policy uncertainty rather than an immediate trade disruption. Companies now confront the likelihood of repeated negotiations and intermittent reviews, which may dampen investment and growth and reduce the probability that the Bank of Canada will feel compelled to tighten monetary policy further.

The Bank of Canada has dismissed concerns that rising energy prices are driving inflation, noting little evidence that higher oil prices are translating into broader price pressures. Coupled with the evolving trade outlook and the central bank’s prudent approach, these factors are fostering a policy orientation that increasingly undermines support for the Canadian dollar.

Market positioning underscores this view. Speculative short positions against the Canadian dollar have risen to their highest level since December, and Canada’s two‑year yield is now more than 140 basis points lower than the U.S. two‑year yield—the widest spread observed since May.

Focus is now on Canada’s June employment report, scheduled for release tomorrow, which could shape expectations for the Bank of Canada’s July 15 meeting. Consensus forecasts anticipate a modest gain of about 10,000 jobs, following May’s unusually large increase of 88,000, while the unemployment rate is expected to stay at 6.6%.

The downside risk is more pronounced: a weaker-than-expected report would deepen the bearish outlook, reinforcing expectations that the Bank of Canada will stay on hold—or even consider easing—while an in‑line or modestly positive report would provide only fleeting relief amid ongoing USMCA uncertainty that continues to dominate Canada’s medium‑term prospects.

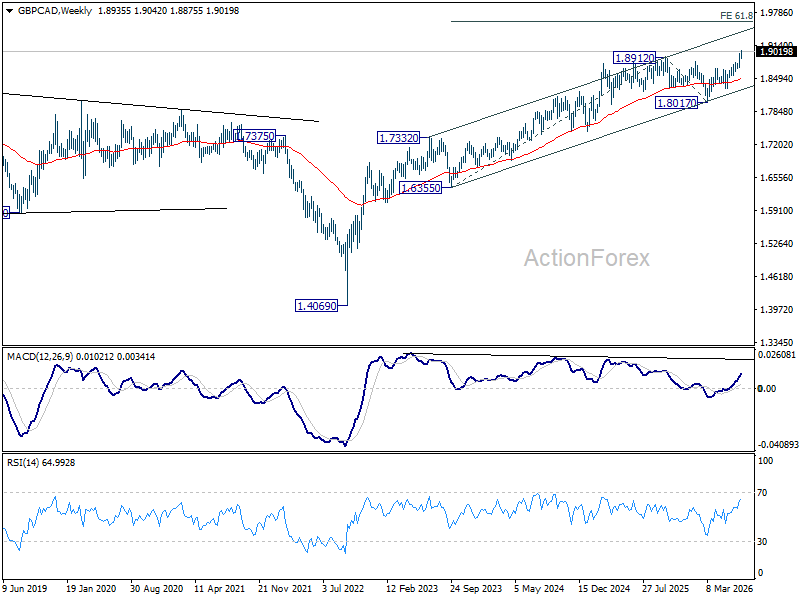

Technically, GBP/CAD is expected to keep rising provided the 1.8875 support level holds. The next key resistance lies at 1.9049. A decisive breach of this level could trigger a sharper upside move, targeting a 138.2% projection derived from the 1.8017‑to‑1.8694 range, implying a potential level near 1.9235. If the 1.8875 support were breached, the bullish case would be postponed and the market would likely enter a consolidation phase.

In the broader context, GBP/CAD is continuing its uptrend that began at the 2022 low of 1.4069. The next medium‑term target is a 61.8% Fibonacci projection of the move from 1.6355 to 1.8912, starting from 1.8017, pointing toward approximately 1.9597.

![Japan’s Kihara Vows Stable Debt Reduction to Secure Market Trust]](https://i0.wp.com/editorial.fxsstatic.com/images/i/japan-001_Medium.jpg?w=1024&resize=1024,1024&ssl=1 "Japan’s Kihara Vows Stable Debt Reduction to Secure Market Trust]")