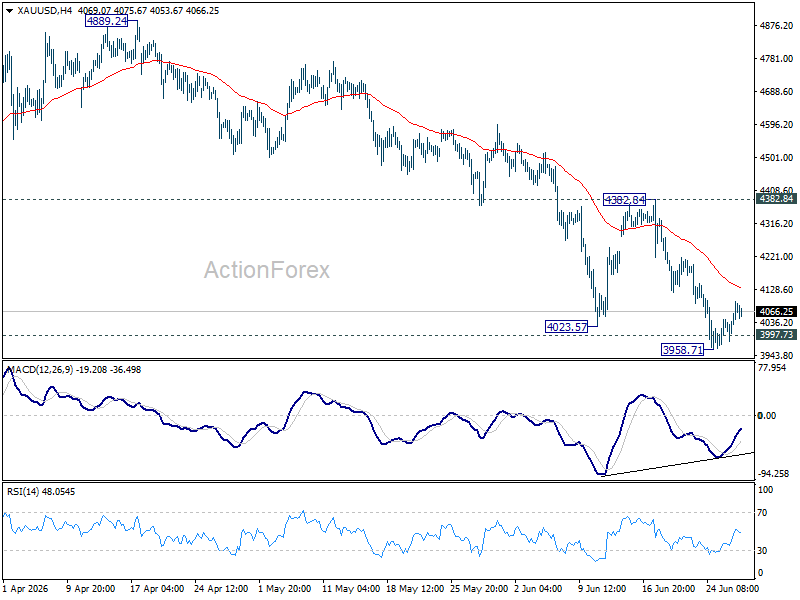

Gold has halted its decline but shows no clear recovery. After briefly dropping below the key $4,000 mark, the metal has clawed back some lost ground. However, the rebound remains tentative and lacks conviction, reflecting market caution ahead of this week’s pivotal U.S. employment data.

The June Non‑Farm Payrolls report, rescheduled for Thursday because of a holiday, carries outsize weight this quarter. Market participants already price in a likely final Fed rate increase this year after Chair Kevin Warsh’s hawkish stance in June. The core question is whether a single hike will suffice. Thursday’s jobs figures could either reinforce that consensus or reignite debate over a second increase, driving divergent moves in the dollar and gold.

Expectations:

Economists forecast payroll growth to moderate to between 115,000 and 130,000 jobs, down from 172,000, while the unemployment rate is seen steady at 4.3% or edging higher to 4.4%. Hourly wages are expected to rise 0.3% month‑over‑month, and annual wage growth to ease from 3.5% to 3.4%. A notable twist this month is the temporary surge in hiring linked to the FIFA World Cup, which may add roughly 40,000 jobs in hospitality, transport and event‑management sectors.

This dynamic makes the report a rare case where the headline figure alone may not capture the full picture. Even if payrolls exceed expectations, a surge driven primarily by temporary World Cup‑related jobs may not signal a durable rebound in labor demand. Consequently, investors will likely focus on wage growth, unemployment trends and broader labor‑market metrics to gauge whether the Fed must tighten policy further.

The scenarios:

If payrolls roughly meet expectations, market participants are likely to stay comfortable with a single Fed rate hike, keeping September as the favored window while treating December as a backup if inflation eases. This scenario would not spark a fresh dollar rally, but it would also avoid a sharp market correction. For gold, the expectation is modest stability rather than a sustained bounce, especially given the upcoming June CPI release two weeks later.

A genuine upside surprise—if accompanied by stronger wage growth—would tell a very different story. It would strengthen the case for a September hike, revive speculation about another move in December, and reinforce the dollar’s medium‑term uptrend. Gold would likely struggle to defend the $4,000 region under those conditions, opening the door to another leg lower.

A downside surprise appears less likely given the World Cup‑related hiring boost, but it cannot be dismissed. Even then, a weaker report is unlikely to overturn the Fed’s tightening bias after several months of resilient employment. Instead, investors would probably shift expectations from September toward December rather than price out additional tightening altogether. That could allow gold to carve out a temporary base between $4,000 and $4,400, but probably not mark the start of a new bull run.

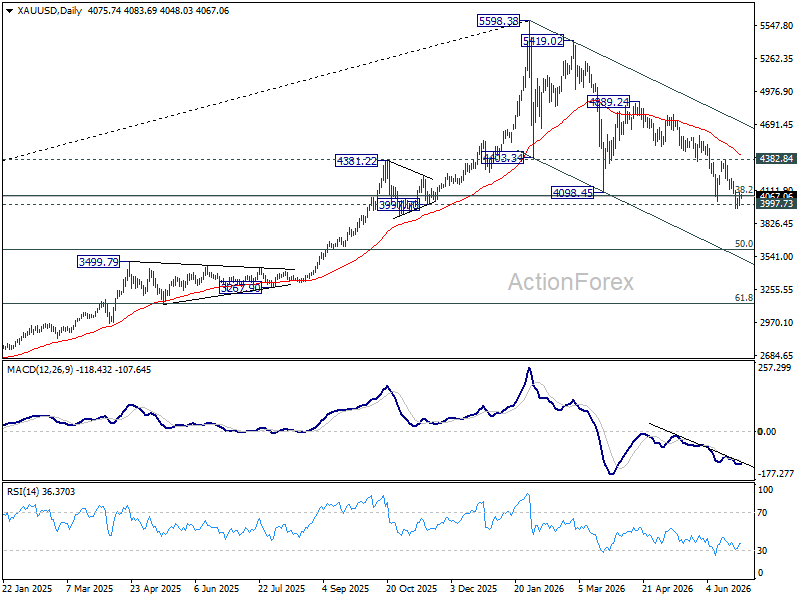

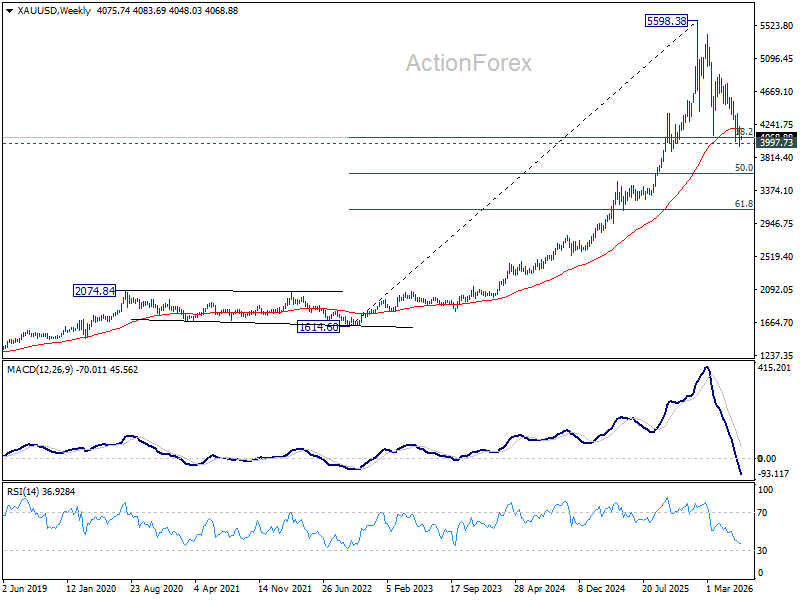

Gold technicals:

Technically, the recent rebound still resembles a pause within a broader down trend. Consolidation above the 3,958.71 temporary low is possible over the near term, but the outlook remains bearish while the 4,382.84 resistance caps upside.

The broader decline from the 5,598.38 record high continues to correct the multi‑year advance from 1,614.60 (2022 low). A sustained break of the 38.2% retracement of the 1,614.60‑to‑5,998.38 move at 4,076.57 would pave the way for the 50% retracement target at 3,606.49.

Also Read

- South Korea’s Massive AI Chip Investment Underscores Persistent Challenges for Crypto Capital Allocation

- Indonesian Rupiah loses ground on Middle East uncertainty

- EUR/JPY Outlook: Gains Above 184.00 Tempered by Bearish Technical Signals and Geopolitical Tension

- Bitcoin ETF Transactions Reach Historic Highs Amid Record-Level Outflows