Markets begin the new week facing two substantial uncertainties: the potential evolution of a proposed US-Iran ceasefire into a formal agreement, and whether upcoming economic data will influence the Federal Reserve’s decision on further rate hikes. Last week, investors eagerly embraced the “peace trade,” with oil prices declining, Treasury yields falling, and equities advancing as markets increasingly anticipated normalized energy flows through the Strait of Hormuz. Despite this optimism, the central agreement remains unsigned.

Over the weekend, new reports indicate continuing negotiation challenges. US President Donald Trump reportedly sought additional modifications to the proposed framework, particularly concerning the reopening of the Strait of Hormuz and the disposition of Iran’s highly enriched uranium stockpile. Iranian negotiators resisted, insisting Tehran would not accept any arrangement failing to fully protect Iranian interests. A White House Situation Room meeting intended to finalize decisions on the framework concluded without resolution, reinforcing the presence of significant obstacles.

President Trump’s statements introduced further uncertainty. While expressing confidence that a deal can eventually be reached, he emphasized he is “in no hurry” and noted military action remains a fallback option should negotiations fail. This combination of patience and threat underscores the risks confronting markets this week. Oil prices have already retreated significantly from their geopolitical premium, with Brent crude falling from above $112 to below $90 per barrel. The current question is whether diplomatic progress can align with market expectations.

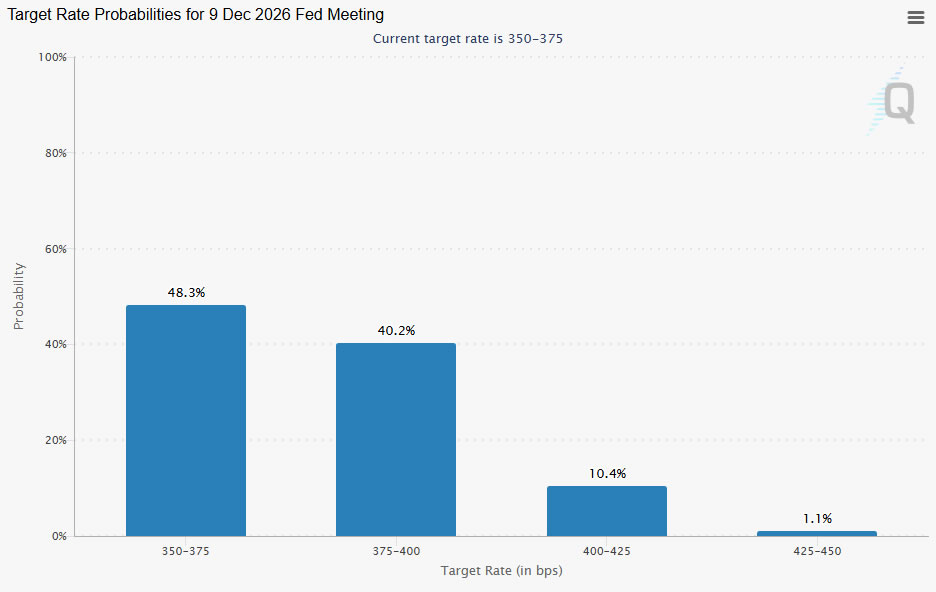

The geopolitical backdrop arrives just as investors confront one of the most significant weeks for US economic data this year. Federal Reserve officials have adopted a more hawkish tone recently, though most have stressed that no immediate rate hike is currently necessary. With Fed funds rates at 3.50%-3.75%, markets have abandoned expectations of rate cuts. The debate now centers on whether the Fed will maintain elevated rates for an extended period or potentially tighten further if inflation pressures persist.

Friday’s Non-Farm Payrolls report stands as the week’s defining economic event. A robust labor market would allow the Fed to maintain focus on inflation risks, particularly if wage growth remains elevated while energy-related cost pressures continue filtering through the economy. Treasury yields and the dollar could respond sensitively to any indications that labor demand remains too strong to comfortably return inflation to target.

Last week’s market trajectory was straightforward: declining oil prices, falling yields, and stronger equities. This week may prove more complex. If diplomatic progress stalls while economic data exceeds expectations, investors may need to reassess both the pace of disinflation and the assumption that the Middle East risk premium has been fully priced out.

Economic Calendar: Inflation, Employment, and Growth in Focus

USD

The US economic calendar dominates the week. Monday’s ISM Manufacturing PMI will receive close attention for signals on industrial demand and, more importantly, the Prices Paid component, which may provide early insight into whether raw material inflation is accelerating again.

Focus then shifts to Wednesday’s ADP Employment Change and ISM Services PMI. While imperfect, ADP serves as a closely watched preview of Friday’s payrolls report, while the services survey will offer perspective on how higher energy costs are affecting the predominant sector of the US economy. Markets will also scrutinize pricing components within the report given ongoing inflation concerns.

Friday’s Non-Farm Payrolls and unemployment rate release represents the main event. Robust hiring and stable wage growth would reinforce the view that the Fed has latitude to maintain restrictive policy and potentially consider tightening if inflation proves persistent. Conversely, weakening employment conditions would reduce pressure on policymakers and likely support the recent decline in bond yields.

EUR

Euro traders face a critical inflation test on Tuesday. ECB officials have spent weeks preparing markets for a June rate hike, and May Flash CPI data is expected to provide the final validation. Consensus forecasts indicate inflation accelerating from 3.0% to 3.3%, which would reinforce the ECB’s concern that higher energy costs are feeding into broader price pressures.

AUD

Australia’s focus shifts to Q1 GDP on Wednesday. Expectations for a June RBA pause are well-established following softer-than-expected inflation data and weaker labor market readings. Consequently, growth data now carries heightened importance. A stronger GDP outcome could revive expectations for another rate hike later this year, likely in August, while weak growth would strengthen the argument that policy tightening is finally beginning to weigh on the economy.

CAD

Canada’s labor market report coincides with US payrolls on Friday, potentially setting off significant USD/CAD volatility. With the Bank of Canada’s June 10 meeting approaching, the employment data serves as the final major policy input. Markets broadly expect the BoC to remain on hold, meaning it would likely require a substantial surprise in either employment or wages to materially alter policy expectations.

Economic Calendar Highlight: Week of June 1, 2026

Date

Currency

Key Event

Mon, June 1

USD

ISM Manufacturing PMI (May)

CHF

Q1 GDP Growth Rate

Tue, June 2

EUR

Flash CPI Inflation YoY (May)

Wed, June 3

AUD

Q1 GDP

USD

ISM Services PMI (May)

USD

ADP Employment Change

Thu, June 4

CHF

CPI Inflation YoY (May)

Friday, June 5

USD

Non-Farm Payrolls (NFP)

USD

Unemployment Rate & Wages

CAD

Employment Change & Unemployment

Also Read

- Franklin Templeton Files for ETFs That Convert Corporate Dividends into Bitcoin Exposure

- Japanese Yen Nears 40-Year Lows as Intervention Speculation Rises

- Europe’s MiCA July deadline puts Binance access and USDT liquidity on the line

- USD/CHF Price Forecast: Fails ahead of 0.8100/YTD peak; bullish potential intact