Last week’s rebound following the US jobs report briefly eased pressure on NZD/USD, yet it has not convinced market participants that the recent downtrend has ended. As the Reserve Bank of New Zealand prepares to announce its policy decision this week, the currency now confronts a pivotal moment that could shape whether the recovery becomes sustainable or merely a temporary pause before further declines.

The RBNZ faces a dilemma, as arguments support both holding rates steady and raising them. Persistently high inflation, exacerbated by this year’s oil price shock, bolsters the case for moving rates back toward neutral sooner. However, domestic demand remains weak, unemployment stays elevated, and easing geopolitical tensions after the US‑Iran ceasefire lessen the immediacy of further tightening.

This split is evident in the policy debate. The NZIER Monetary Policy Shadow Board leans toward keeping the Official Cash Rate unchanged at 2.25%, though it describes the July meeting as an exceptionally close call. Proponents of a rate hike emphasize ongoing inflation pressures, whereas opponents contend that the lingering impact of the recent energy shock and slowing domestic activity warrant waiting for clearer guidance. Notably, most participants agree on the medium‑term trajectory, anticipating the OCR to rise toward 3.00%‑3.25% within the next year.

Major banks’ forecasts echo the same theme. ANZ and BNZ project a 25‑basis‑point increase this week, with ANZ urging a balanced approach to guidance to prevent policymakers from becoming overly aggressive should data deteriorate. BNZ concurs that inflation risks remain elevated despite recent geopolitical improvements.

Conversely, ASB and Westpac anticipate the RBNZ will hold rates steady. ASB has revised its earlier July hike forecast following the de‑escalation of Middle East tensions, while Westpac expects greater consensus among policymakers to wait, as they consider the need to monitor inflation pressures that may persist after the energy shock.

Consequently, market participants are likely to focus less on the headline outcome and more on subsequent developments. A hold that merely postpones a future hike could curb downside pressure on the kiwi, while a 25‑basis‑point increase paired with muted forward guidance may not sustain gains. Investors will scrutinize signals about the speed of the RBNZ’s return to neutral policy rather than viewing this week’s decision in isolation.

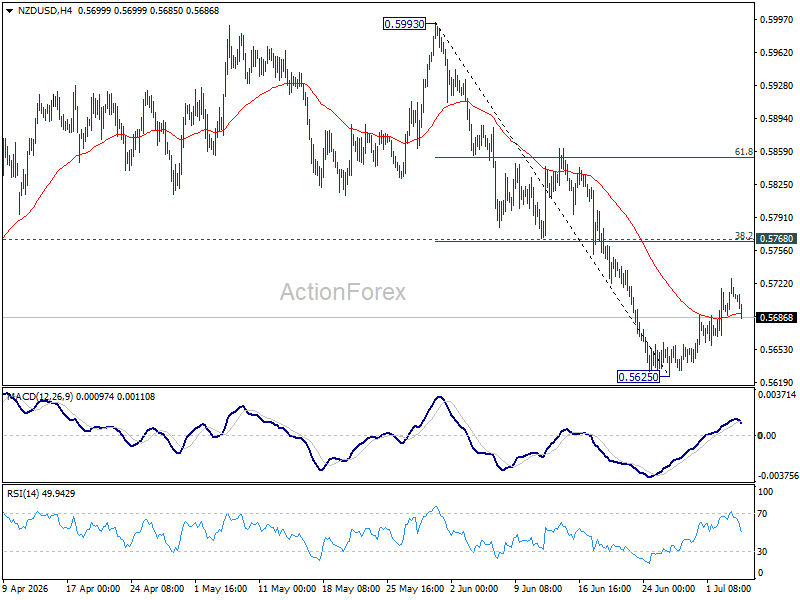

Technically, NZD/USD remains vulnerable. The recent bounce stemmed primarily from broad USD weakness following a softer US employment report, not from a substantive improvement in New Zealand’s fundamentals. While the 0.5768 resistance cluster (the 38.2% retracement of the 0.5993‑to‑0.5625 range at 0.5766) continues to limit upside, the short‑term outlook stays biased downward. A breach below 0.5625 could reignite the decline from 0.6092 toward the 0.5579 structural support level.

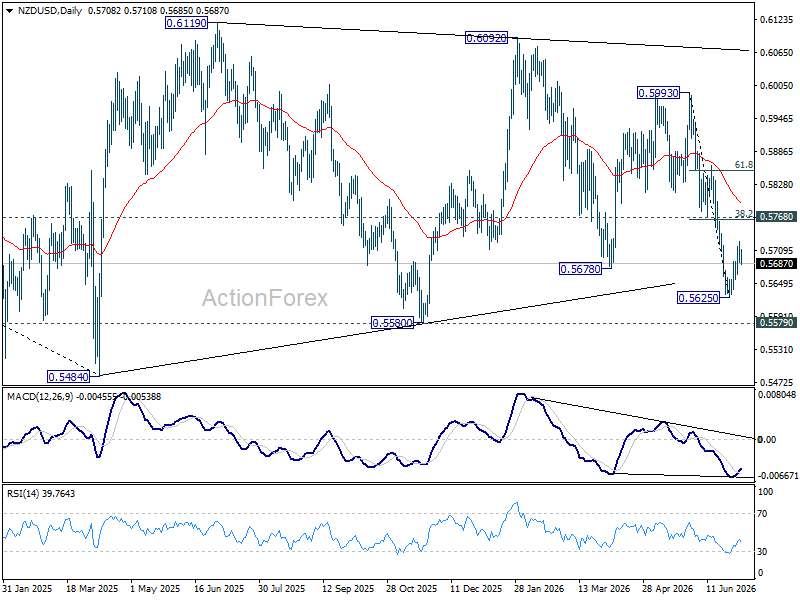

The longer‑term chart reinforces the prevailing bearish trend. Price movement from the 2025 trough at 0.5484 remains a corrective phase within the extended downtrend that began at the 2021 high of 0.7463. Although momentum has not yet signaled a definitive bearish breakout, continued trading beneath 0.5625 would indicate that the correction is complete and raise the probability of another test of the 2025 lows.

Also Read

- EUR/JPY Holds Ground Near 185.00, Targets Symmetry Triangle Upper Vertex

- Rising Momentum Drives XRP Price Upward as Breakout Tests New Support

- ECB Official Emmanuel Moulin Says Bank Is Well-Positioned After June Rate Hike

- New Zealand Dollar Slips as NZIER Divided on July Rate Path; Hike to 3.00-3.25% anticipated over Next 12 Months