Three major central bank meetings headline a pivotal week, but all eyes remain on the inflation wildcard and its implications for monetary policy trajectories.

Last week’s stronger-than-expected employment figures reinforced the view that the Fed can maintain its primary focus on inflation. With labor market dynamics no longer demanding immediate attention, investors are increasingly weighing whether elevated energy prices will ultimately necessitate additional rate hikes later this year.

Against this backdrop, Wednesday’s U.S. CPI report emerges as the week’s most critical event, poised to influence Treasury yields, currencies, and global equity markets. The ECB follows closely, though attention centers on updated forecasts rather than the already-priced rate increase. Meanwhile, the Bank of Canada confronts a starkly different landscape as policymakers weigh domestic recessionary pressures against transient, oil-driven inflation spikes.

The U.S. inflation report will likely establish global market sentiment. Following three consecutive months of robust payroll growth, the labor market no longer provides grounds for easing. This dynamic affords Fed officials increased flexibility to monitor inflation developments and the pass-through effects of higher energy costs.

Market consensus projects headline CPI accelerating from 3.8% year-over-year to 4.2% in May, while core CPI is expected to rise modestly from 2.8% to 2.9%. Although headline inflation increases are anticipated due to energy costs, scrutiny will intensify on the core reading. Any upside surprise in core inflation could reinforce expectations for further tightening, driving Treasury yields and the dollar higher while pressuring equity valuations.

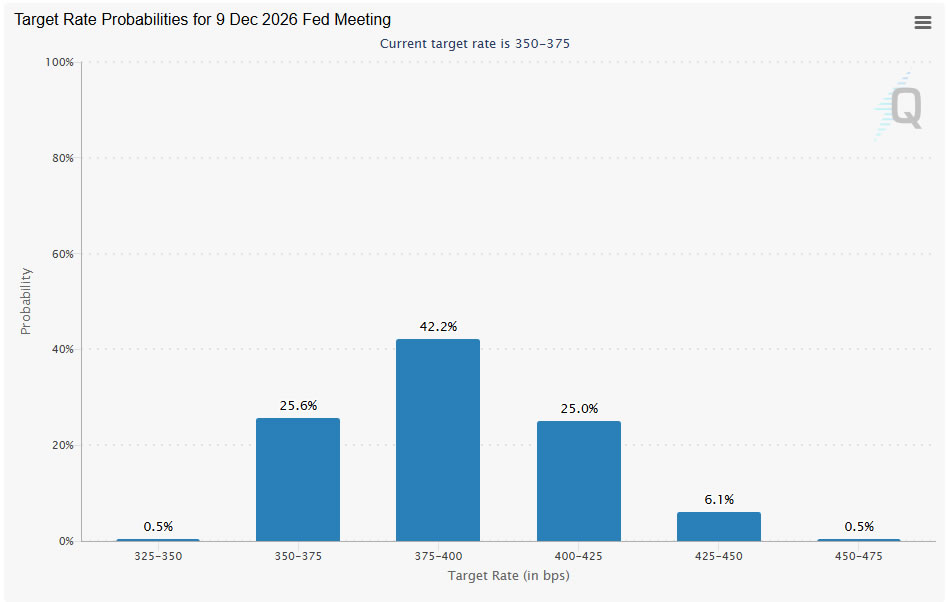

The market reaction function has evolved significantly over the past month. Rate cut expectations have effectively been dismissed, with Fed funds futures now implying nearly a 75% probability of at least one additional rate increase by year-end. The CPI report thus serves as a critical test of whether these expectations hold water.

For the ECB, a 25 basis point deposit rate increase to 2.25% is widely anticipated. Since the decision is fully priced in, market focus will shift to President Christine Lagarde’s guidance and, more critically, updated staff projections. Recent PMI surveys have painted an increasingly challenging Eurozone growth picture, raising recession concerns amid persistent inflation pressures.

Nonetheless, Lagarde is likely to strike a measured tone, acknowledging upside inflation risks while highlighting growing economic activity concerns. Markets should not expect aggressive forward guidance. Instead, the new projections may provide the clearest policy signal. Upward revisions to near-term inflation forecasts paired with 2026 growth downgrades toward the 0.3%-0.5% range would reinforce the emerging stagflation narrative across Europe.

While a Reuters survey revealed that over 60% of economists expect one additional ECB rate increase in September, conviction remains tepid. Weaker growth confirmation could cap euro appreciation even with a retained tightening bias.

The Bank of Canada enters the week from a substantially different vantage point. Canada has already recorded two consecutive quarters of contraction, meeting the technical recession criteria. Consequently, the central bank’s policy stance diverges markedly from both Fed and ECB approaches.

Recent employment data have provided policymakers some leeway. Strong May job growth alleviated immediate easing pressure and supports the Bank’s decision to maintain current rates. Simultaneously, officials have repeatedly indicated willingness to look through temporary inflation increases driven by energy prices, asserting that domestic weakness should absorb part of the impact.

A pause at 2.25% is widely forecast. Per Reuters polling, over 80% of economists anticipate rates remaining unchanged through year-end. The policy statement and press conference will likely reinforce the hold pattern, albeit uncomfortably, as the Bank balances recession risks against temporary inflation pressures.

Weekly Highlights:

- Tue, June 9: AUD – Consumer & Business Confidence

- Wed, June 10: CNY – China CPI & Trade Balance

- Wed, June 10: USD – US Consumer Price Index (CPI)

- Wed, June 10: CAD – BoC Rate Decision

- Thu, June 11: EUR – ECB Rate Decision

- Thu, June 11: USD – US Producer Price Index (PPI)

- Fri, June 12: GBP – UK GDP

- Fri, June 12: USD – U. of Michigan Consumer Sentiment (Prelim)