Key Canadian Developments

- The Bank of Canada maintained its policy rate at 2.25%. While soft growth suggests further tightening is unwarranted, persistent inflation risks keep rate cuts off the table, supporting an extended hold.

- Canada’s trade balance strengthened, moving deeper into surplus territory. Robust export gains and higher volumes indicate that net trade will support Q2 growth after weighing on Q1.

- A rebound is anticipated in Q2, though ongoing uncertainty will limit the upside.

Key U.S. Developments

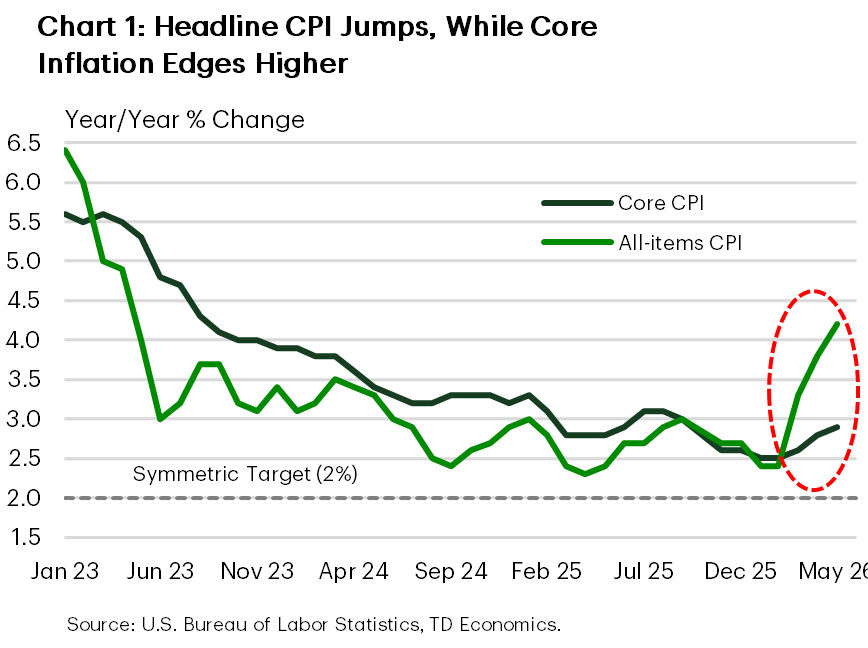

- The impact of the Iran conflict was reflected in May’s CPI report, which rose to a three‑year high. Core inflation increased to 2.9% year‑over‑year, matching consensus forecasts.

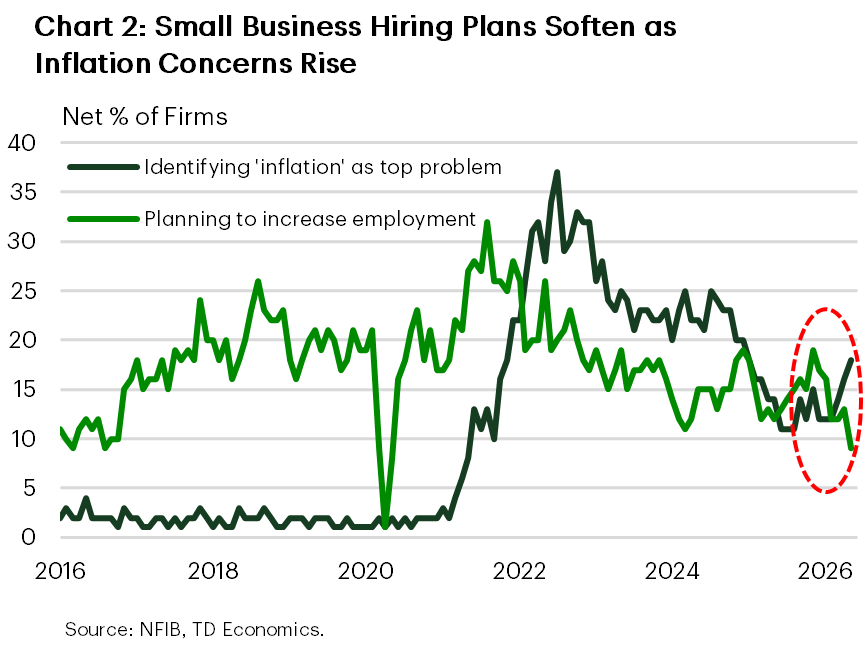

- NFIB pricing indicators also rose in May, and inflation concerns intensified, while hiring plans continued to weaken.

- Existing home sales exceeded expectations in May, yet activity remains below historical norms. Home price growth, at 1.3% year‑over‑year, remains modest.

Canada – Tumbling Energy Prices and Economic Stabilization

After a weak first quarter, the housing market is showing tentative signs of stabilization. Housing starts fell 6% month‑over‑month in May, yet remain above Q1 levels, limiting the downside to residential investment in the second quarter. Existing home sales increased 5.5% month‑over‑month in May, with gains in most provinces. New listings declined, pushing the sales‑to‑new‑listings ratio to 49.2%. Although still below historical averages, this indicates a more balanced market. Prices remain mixed, with continued weakness in segments such as condos. The improving alignment between buyers and sellers is supporting a partial rebound in activity, suggesting firm Q2 sales growth. Overall, elevated inventories and slower population growth remain headwinds, but the near‑term outlook points to stabilization rather than further decline.

While emerging stability in the housing market is encouraging, consumer spending remains soft amid rising inflation. Retail sales rose 0.5% month‑over‑month in April, but volumes were unchanged, indicating that higher prices are driving the increase (Chart 1). Strength in automobiles and gasoline obscured underlying weakness, as core retail sales declined for a second consecutive month, falling 0.7% month‑over‑month. This suggests households are becoming more selective as higher energy costs strain budgets. Consequently, consumer spending is expected to grow modestly in Q2, with the recent decline in energy prices providing some relief in the latter half of the year.

Attention now turns to next week’s inflation report for May. A firm reading is expected, with gasoline prices projected to rise about 3% over the month. The primary focus will be on inflation breadth (Chart 2) and core measures. In April, headline inflation increased to 2.8% year‑over‑year due to higher energy prices, while the Bank of Canada’s core measures averaged 2.1%. The key question for the BoC is whether price pressures are spreading beyond energy and, given limited upside to oil prices, how persistent any pass‑through effects may be.

Overall, the upcoming inflation report will be crucial for assessing underlying pressures, but the broader backdrop features excess supply, subdued domestic demand, and likely moderating energy prices. These factors should limit pass‑through to core inflation, keeping the Bank of Canada on hold for the remainder of the year.

U.S. – Price Pressures Now on the Front Foot

Middle East tensions spiked earlier in the week and then moderated, as President Trump threatened new strikes on Iran before reversing course, citing progress toward a deal. WTI oil prices, which had hovered near $90 per barrel, fell sharply toward $85 per barrel. The 10‑year Treasury yield initially dipped, reflecting hopes that a resolution would curb the energy shock’s spillover into broader inflation expectations, but later recovered as investors absorbed another firm inflation report.

The May CPI report provided the clearest evidence that inflation pressures are building. Headline inflation rose to 4.2% year‑over‑year, the fastest pace in three years (Chart 1). Higher energy costs drove most of the increase. Core inflation, though more restrained, still rose to 2.9% year‑over‑year, keeping the overall rate above target and reinforcing a “higher for longer” policy stance. While shelter inflation eased after April’s outsized gain and core goods prices slipped, non‑housing services remained strong.

Inflation pressure was also evident in the NFIB small‑business survey, where an increasing share of firms reported raising average selling prices and planning further increases in the coming months. This suggests that higher energy and input costs are beginning to affect broader price levels.

Housing provided a modest reprieve from the bleak inflation news. Existing home sales rose 3.2% in May, reaching the highest level since December. Nonetheless, overall activity remains near the 4‑million mark for a third consecutive year, with home price growth staying modest.

Labor market signals were mixed. Initial jobless claims rose for the third consecutive week but remained within a narrow range, while continuing claims stayed low by historical standards. Small‑business survey data, however, were less reassuring, indicating slower job creation ahead, with job openings and hiring plans weakening amid rising inflation concerns (Chart 2).

In summary, the ongoing effects of the Middle East conflict continue to appear in the data, making it increasingly difficult for the Fed to ignore. We expect core inflation to remain elevated through year‑end, supporting a prolonged Fed pause. Next week will mark Kevin Warsh’s inaugural FOMC meeting as Chair. Market participants will scrutinize not only a clear rate signal but also cues regarding his communication approach. Warsh has signaled a preference for a communication shift, possibly forgoing a press conference after each meeting. We anticipate the committee will signal a “higher for longer” stance in its updated Summary of Economic Projections, which previously indicated 25 basis points of easing for this year and next, and will likely remove its easing bias from the statement. This shift should bring the Fed closer to market pricing, which currently reflects a near‑even split between “no action” and a 25‑basis‑point hike by year‑end.