Yen rose broadly today after Finance Minister Katayama indicated that Tokyo aims to urge pension funds—including the Government Pension Investment Fund (GPIF)—to boost allocations to domestic financial assets. Although no official policy shift was declared, investors viewed the remarks as a possible move to tackle one of the yen’s long‑standing structural issues: continual capital outflows toward foreign assets.

The impact spread beyond FX markets. Japanese government bonds surged across the yield curve, with the 20‑year yield slipping 11.5 basis points to 3.75%, the 10‑year yield easing 10 basis points to 2.775%, and the 30‑ and 40‑year yields each dropping more than 8 basis points.

From FX Intervention to Capital‑Flow Management

The market’s reaction underscores the magnitude of Japan’s institutional investor base. GPIF, the globe’s largest pension fund with roughly ¥292.6 trillion in assets, has kept a roughly even split between domestic and overseas bonds and equities since its landmark portfolio redesign in 2014.

This tilt away from Japanese assets has produced a decade of structural capital outflows, with hundreds of trillions of yen swapped for foreign currencies to buy overseas holdings. Katayama’s remarks were thus seen as hinting—though cautiously—at a potential partial reversal of that trend.

Drivers Behind the Strong Market Reaction

Such a shift could bolster the yen via two mechanisms:

- First, a larger tilt toward domestic assets would necessitate converting some existing foreign‑currency holdings back into yen, generating structural demand for the currency without relying on direct intervention.

- Second, heightened demand for Japanese government bonds would lend extra long‑term support to the JGB market, especially as investors grow wary of rising long‑end yields and Japan’s fiscal outlook. Encouraging more domestic investment could therefore bolster the yen while alleviating upward pressure on government borrowing costs.

More broadly, the idea aligns with Japan’s effort to find alternatives to traditional FX intervention. Given that the Fed‑BoJ interest‑rate differential remains around 250‑275 basis points, aggressive BoJ tightening is unlikely in the near term. Targeting capital flows provides policymakers with an additional tool to temper structural yen weakness without depending solely on rate hikes or spot‑market intervention.

A Conceptual Move, Not Yet Formal Policy

Still, today’s market reaction could be premature if no concrete steps follow. Katayama merely urged greater domestic investment without unveiling any formal portfolio adjustments. GPIF is governed by an independent board tasked with maximizing long‑term returns, and its strategic asset allocation is generally reviewed only during its multi‑year planning cycle, not in reaction to ministerial remarks.

Markets have witnessed comparable episodes before—such as last week’s speculation about a shift in Japan’s intervention approach, which dissipated when no policy action ensued. Furthermore, even a substantial reallocation by GPIF would not erase the sizable interest‑rate gap that continues to drive global carry trades against the yen.

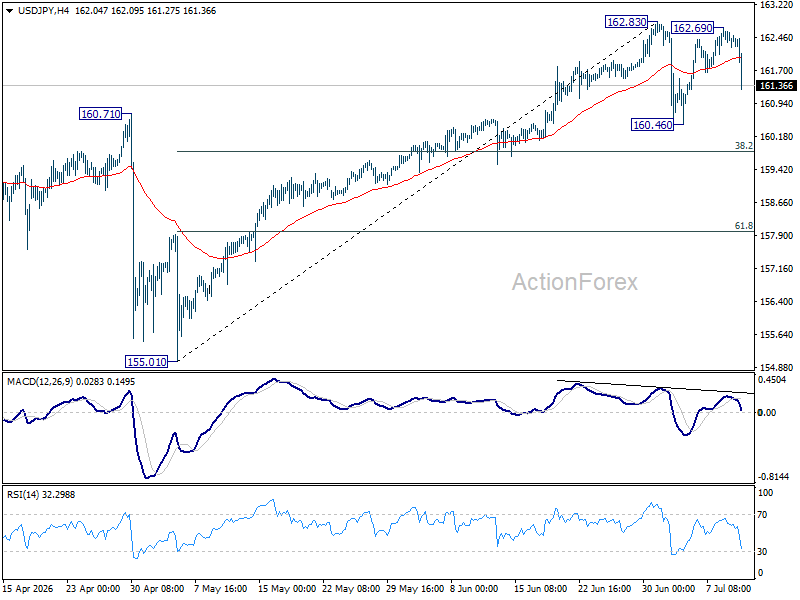

USD/JPY Continues Its Consolidation Phase

Technically, the steep drop in USD/JPY confirms that the bounce from 160.46 ended at 162.69 after being rejected at the 162.83 high. The broader picture, however, stays the same.

The fall from 162.83 is interpreted as the third leg of a consolidation pattern nested inside the broader uptrend originating from 155.01. A deeper retracement could test 160.46 or lower, but solid support is anticipated near the 38.2% retracement of the 155.01‑162.83 move—around 159.84—to cap the downside. The longer‑term upward trend is expected to resume later, merely postponed.