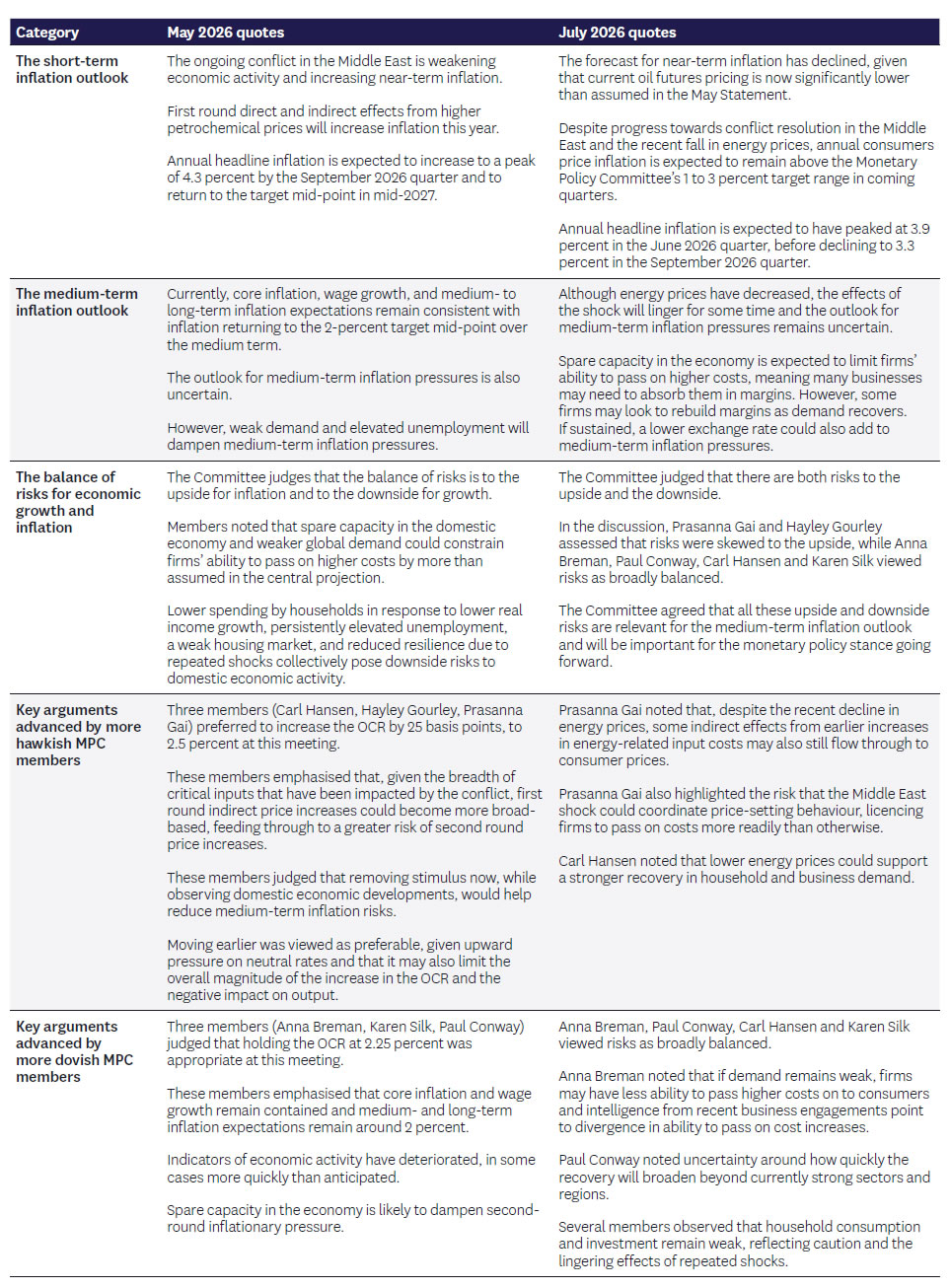

- The RBNZ raised the Official Cash Rate (OCR) by 25 basis points to 2.5%, a decision reached by consensus and requiring no separate vote.

- The Monetary Policy Committee’s (MPC) balance remains unchanged, with Gai, Gourley and Hansen viewed as hawks while Breman, Conway and Silk retain a more dovish stance.

- A key justification for the increase was the concern that leaving the OCR unchanged could have allowed financial conditions to ease further, potentially through lower rate expectations and a weaker exchange rate.

- The MPC appears comfortable with an end‑2026 OCR level in the 2.75‑3.0 % range, broadly consistent with its May forecasts.

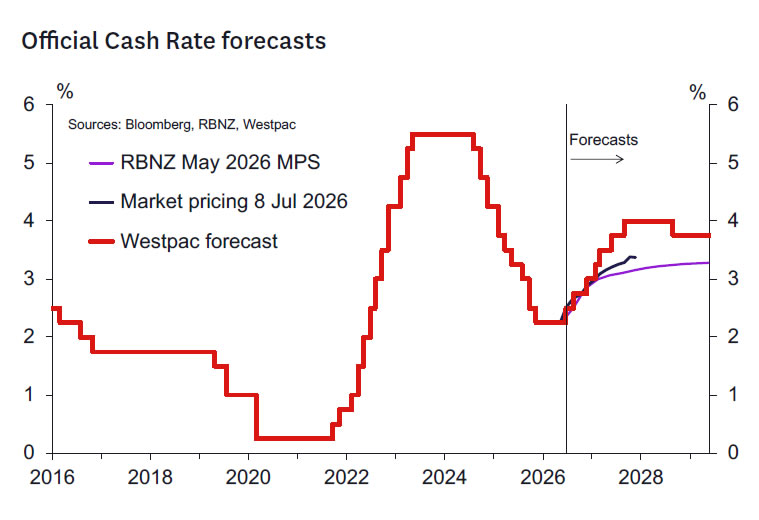

- Westpac expects two additional 25bp hikes at the September and December 2026 meetings, followed by incremental increases through 2027. The peak OCR of 4.0 % is now projected for September 2027 rather than December 2027.

OCR Raised by 25bps to 2.50%

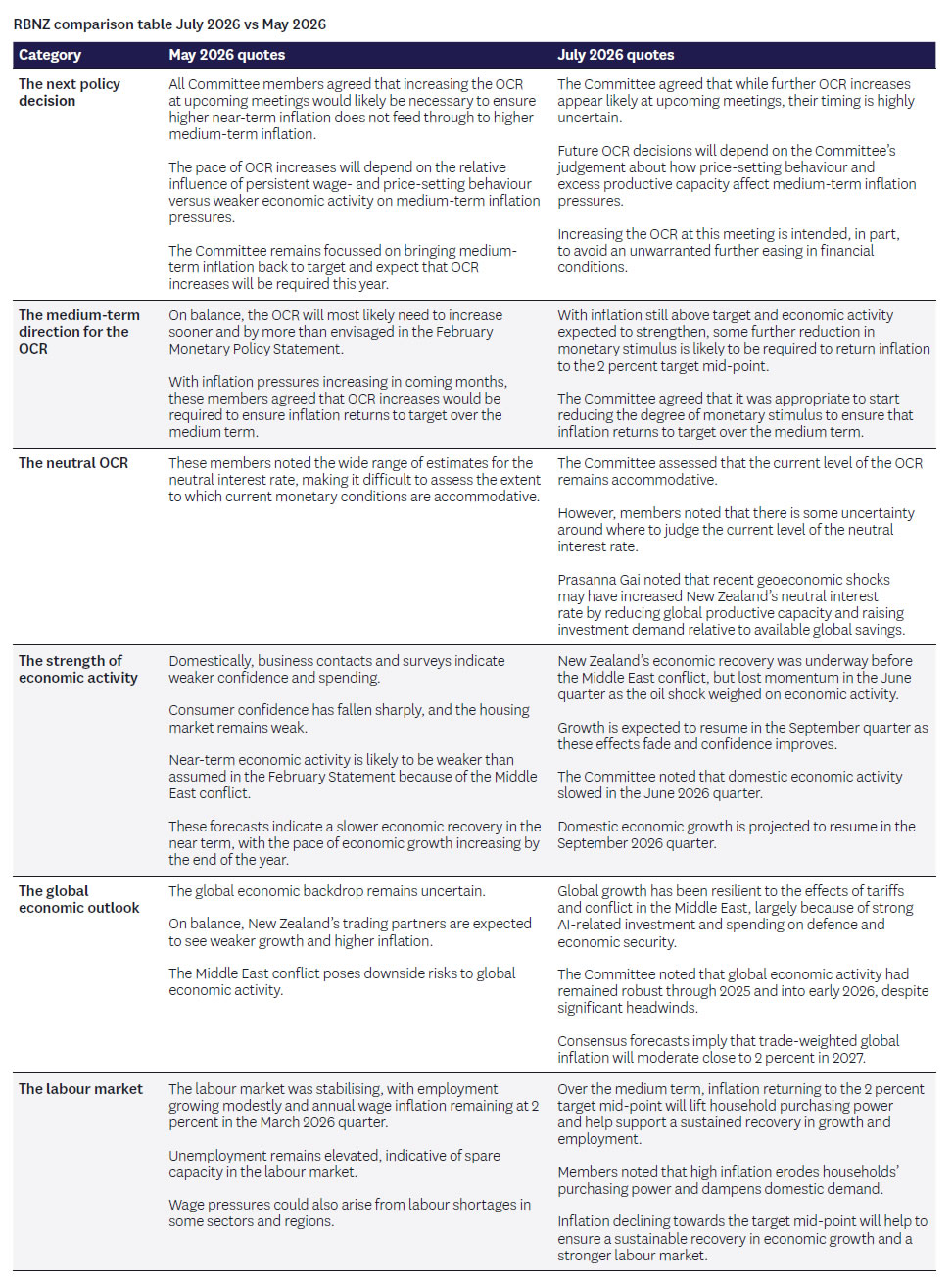

Today the Reserve Bank of New Zealand (RBNZ) lifted the OCR by 25 bps to 2.5 %, marking a shift from earlier expectations of an “on‑hold” outcome. The decision was unanimous, with no formal voting split disclosed.

The Bank acknowledged the recent decline in oil prices and the accompanying easing of inflationary pressures. Its latest forecasts now show annual inflation at 3.9 % in Q2 and 3.3 % in Q3—slightly lower than previous projections but still above the 2 % target, justifying further tightening.

Global growth risks have stabilised compared with May, when energy price spikes created greater uncertainty. Nonetheless, the RBNZ highlighted that financial conditions could have eased further if the OCR had been left unchanged, prompting today’s hike.

The policy outlook points to additional tightening in upcoming meetings, though the precise timing remains uncertain. The Bank aims to return the OCR to a neutral zone, currently viewed as being in the low‑3 % range. However, officials note that the neutral rate may be shifting higher in response to persistent inflation and evolving geopolitical conditions.

Deputy Governor Prasanna Gai warned that the neutral OCR could rise amid heightened geopolitical uncertainty, while Paul Conway observed that short‑term inflation expectations are pushing the neutral rate upward. The MPC’s internal balance stays the same, with Gai, Gourley and Hansen maintaining a hawkish tilt and Breman, Conway and Silk retaining dovish positions.

The RBNZ’s forward guidance has broadened. In May the focus was on second‑round price pressures, rising inflation expectations and wage dynamics. Those factors remain relevant, but officials now also cite signs of strengthening domestic and global growth, as well as trends in financial conditions—including the exchange‑rate channel—as key considerations for future moves.

In a technical update, the Bank announced it will bring forward the full runoff of its LSAP portfolio to June 2027. This adjustment carries no monetary‑policy implications and is described as a routine operational change.

Westpac Outlook – 4% Peak in the OCR Reached a Little Earlier in 2027

Westpac continues to anticipate the two 25bp OCR hikes it forecast before today’s meeting—scheduled for the September and December 2026 deliberations. These steps will lift the year‑end OCR to 3.0 %, slightly higher than previously projected. Beyond 2026, Westpac retains its forecast of a 4.0 % peak, now expected at the September 2027 MPS meeting rather than December 2027.

Given the current uncertainty, the Bank emphasises that the precise path of tightening will depend on both global developments and domestic data releases. As such, the September 2026 increase should not be regarded as a “done deal.”

Things to Watch Ahead of the 2 September Meeting

The next policy review is slated for 2 September, when the RBNZ will publish a full Monetary Policy Statement and refreshed economic forecasts. The evolving stance will hinge on the trajectory of the Middle‑East conflict and its impact on New Zealand’s inflation and growth outlook.

A number of high‑profile domestic indicators will be released between now and September, offering insight into inflationary pressures and economic momentum:

- Q2 CPI (21 July) and July Selected Prices (17 August) – gauge whether energy‑price shocks are feeding into broader price indices.

- Q3 RBNZ surveys (13, 14 and 21 August) – track inflation expectations from professional forecasters, households and businesses.

- Q2 QSBO (14 July) and July/August ANZ Business Outlook (30 July/31 August) – assess early versus late survey responses and business sentiment.

- July/August PMI and PSI surveys (mid‑July/mid‑August) – provide early signals on Q3 GDP growth.

- Q2 labour market surveys (5 August) – examine employment, hours worked and underlying inflation pressure indicators.

Additional high‑frequency data—such as filled job counts, consumer spending, building consents, housing market activity, job ads and confidence measures—will also be monitored. The RBNZ will keep a close eye on price movements for New Zealand’s key export commodities, as these can influence inflation dynamics and the exchange rate.