- US CPI report and Fed Chair Warsh’s dual testimonies in focus.

- Headline inflation expected to ease, but market awaits actual deceleration.

- Warsh’s rhetoric scrutinized for signals on potential September rate hike.

- Euro/dollar could revisit recent lows if CPI or Warsh’s remarks prove hawkish.

Dollar Continues Strong Run

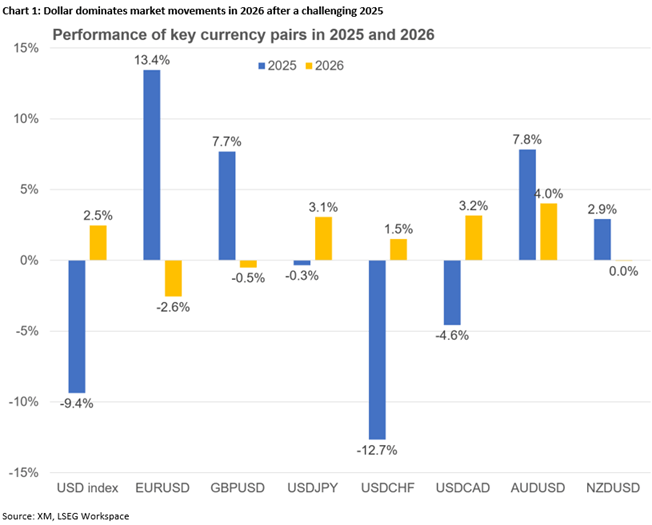

The US dollar has emerged as a key driver in 2026, with Fed Chair Warsh’s appointment bolstering bullish sentiment. The dollar index reached its highest level since May 2025 in late June, signaling renewed strength following a recovery from earlier trade dispute impacts.

CPI Data in Focus Ahead of Policy Meeting

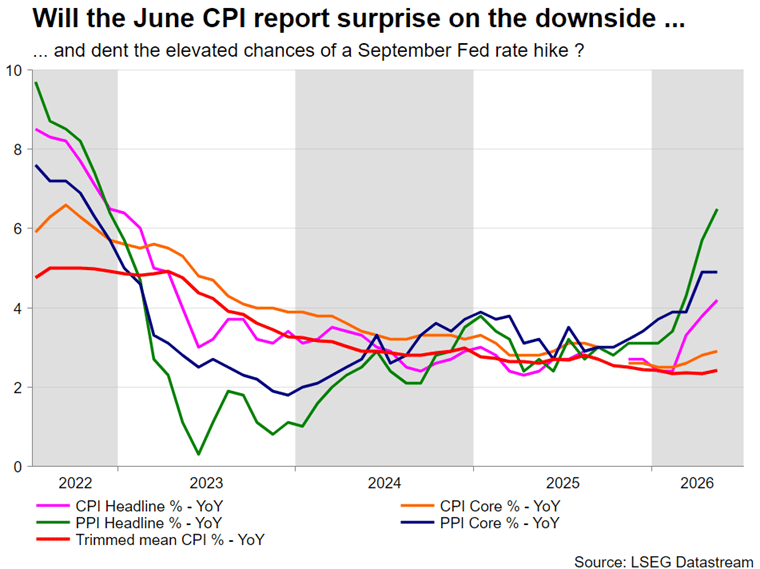

Next week’s data calendar includes the latest CPI report on Tuesday at 12:30 GMT, preceding the July 29 FOMC meeting. Following May’s rebound, headline CPI is projected to ease below 4% again, erasing part of the prior month’s spike, driven by a 20% monthly oil price decline in June. Core CPI is similarly expected to moderate, though both metrics remain above the 2% target.

Additional data points include PPI on Wednesday and retail sales on Thursday, with the University of Michigan Consumer Sentiment index concluding the week. China’s recent PPI performance sets a benchmark, while lower energy prices and World Cup spending are likely to buoy retail sales and sentiment figures.

Warsh’s Testimony Sets Tone

Fed Chair Warsh will deliver back-to-back testimonies before the House Financial Services Committee on Tuesday and the Senate Banking Committee on Wednesday, both starting at 14:00 GMT. His remarks are critical for gauging future policy direction, particularly regarding September rate hike probabilities.

Since assuming office, Warsh’s communications have reinforced a hawkish tilt. His post-FOMC press conferences, speeches at the ECB Forum, and the June 17 minutes signaled renewed inflation focus and skepticism toward forward guidance. He has openly criticized predecessor Alan Greenspan’s inflation management and linked current policy decisions to an overvalued balance sheet.

Barring unexpected hawkish signals, market attention will center on Warsh’s assessment of the labor market and incremental hints about September policy adjustments. A confident tone on employment could strengthen expectations for further tightening.

Warsh may reiterate his previous statements, emphasizing persistent inflation risks and potential critiques of past policy approaches. Should labor market data remain resilient, his commentary could further cement expectations for anticipated rate hikes in September.

Euro/Dollar Faces Volatility

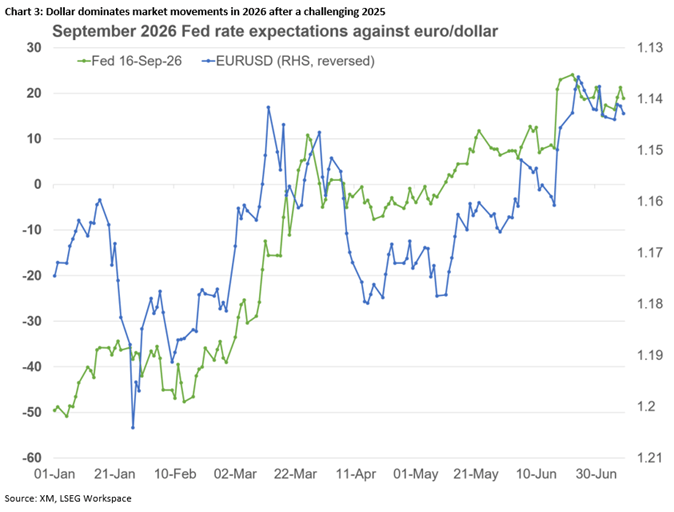

Following the June FOMC meeting, the euro/dollar pair broke free from its 1.1470–1.1829 range, reaching its lowest mark since May 30, 2025. The eurozone’s economic struggles and the ECB’s limited impact on the currency have amplified dollar strength.

A softer CPI print and neutral Warsh commentary might temporarily weaken the dollar’s appeal. However, expectations for a September rate hike are likely to persist. A test of the lower range boundary at 1.1470 could occur, though such a dip may be fleeting. Conversely, persistent inflation and hawkish rhetoric could push the pair toward the recent trough of 1.1324.

Also Read

- Technical Analysis Suggests XRP Could Target $7 by Year-End Despite Recent Weakness

- Judge lets Terraform use Jump lawsuit evidence while blocking four late creditor claims

- Leading Crypto Firms Launch ‘Internet Court’ to Resolve AI Agent Disputes

- Bitcoin is “A Screaming Buy”: Standard Chartered Backs $100,000 Target, Shrugs Off Strategy (MSTR) Sell-Off

Sell-Off")